Corporate Strategy

Delivering on our Strategic Objectives

Message from the Chief Executive

"Mindful of the dynamic context, we will maintain our disciplined approach to the execution of our strategic plans …"

We registered excellent results for the year ended June 2019, with further headway made at the level of both the banking and nonbanking clusters, more particularly on the international front. Profit attributable to equity holders grew by 31.3% to reach Rs 9,482 million, with the combined share of foreign-sourced income and non-banking operations standing at 69% thereof. As a result, earnings per share rose from Rs 30.26 to Rs 39.70.

Underpinned by our diversification strategy, operating income increased by 19.3% to reach Rs 20,226 million. This was supported by a growth of around 21% in net interest income, which benefitted from enhanced performances across banking subsidiaries. In particular, MCB Ltd registered a significant expansion of its international loan book and improved yields on Government securities. Net fee and commission income grew by 10% to reach Rs 3,786 million as a result of enhanced contribution from MCB Capital Markets Ltd and higher revenues across banking subsidiaries, with strong growth recorded with regard to our Energy and Commodities business and payments services. In spite of a subdued performance in respect of profit on exchange and lower gains on disposal of investments by MCB Equity Fund Ltd, ‘other income’ grew by 25%, principally due to fair value gains on equity instruments at the level of MCB Ltd and higher contribution from entities in the non-banking segment, mainly MCB Consulting Services Ltd and MCB Real Assets Ltd.

On the back of initiatives to strengthen our human capital and uplift our technological readiness, operating expenses increased by 10.4%. Yet, in view of our robust performance on the revenue front, our cost to income ratio declined by 3.0 percentage points to 37.1%.

Whilst the Group’s impairment charges rose by some 20%, the cost of risk in respect of loans and advances dropped marginally to 59 basis points of the latter. Asset quality further improved as gauged by our gross NPL ratio declining from 4.5% to 4.1%.

Notwithstanding a reduced contribution from Banque Française Commerciale Ocean Indien, Group results have also been supported by an increase of Rs 97 million in our share of profit of associates, explained by better performances by Société Générale Moçambique and Promotion and Development Group.

As another source of satisfaction, the Group has maintained robust foundations for the achievement of sound and sustainable business growth. We posted an improvement in our capital adequacy ratios, alongside maintaining healthy funding and liquidity positions.

Thanks to our sound credentials, Moody’s Investors Service has upgraded the rating of MCB Ltd from Baa3/P-3 to Baa2/P-2. The agency acknowledged the Bank’s disciplined and prudent expansion strategy, notably in Africa. Today, MCB exhibits the best long-term deposit rating amongst African commercial banks rated by the agency. We are confident that our improved credit profile will be a key element in assisting the Bank to further deepen and widen its regional footprint. In addition, as a testimony of the strong market confidence in our core fundamentals, MCB Ltd has, in April last, successfully secured a USD 800 million Dual Tranche Syndicated Term Loan Facility. This facility attracted commitments in excess of USD 1 billion from 24 participating banks spanning Europe, the Middle East and Asia. It represents the largest-ever syndicated facility in our history and marked our return onto the international debt markets after some 13 years.

On the domestic front, MCB Ltd has consolidated its leadership position, while effectively responding to the needs of its individual andcorporate clients. Toward this end, the Bank has continuously enriched its value proposition, underpinned by notable inroads made as regard its digital transformation and further innovation on the payments side. Beyond, the Bank has pursued its regional diversification agenda, with a significant expansion in exposures posted in respect of Energy and Commodities financing and international structured finance. The Group’s foreign banking subsidiaries have pursued their business strategies across targeted markets, backed by an improved range of solutions, increased brand visibility and reinforced capabilities.

As for our non-banking entities, they expanded their activities and were increasingly involved beyond our local shores. While MCB Leasing Ltd and MCB Factors Ltd have maintained their prominent market positioning, MCB Capital Markets Ltd upheld its growth momentum in spite of the challenging operating environment. It completed a number of capital raising transactions locally and was increasingly active in advising African clients on their financing initiatives. The MCB range of funds, especially the USD-denominated fixed income funds, performed strongly relative to comparable funds, while assets under management increased year-on-year to reach USD 814 million despite a competitive environment. Indeed, the MCB Africa Bond Fund was ranked the top performing fund over a 3-year and 5-year horizon among more than 50 Africa focused funds tracked by Africa Global Funds.

Group entities have been

actively reinforcing

their foundations in order

to be in a position

to support sound

and sustainable growth.

Spanning the organisation as a whole, further progress has been made in showcasing our ‘Bank of Banks’ proposal aimed at positioning the Group as a regional hub for handling trade finance, payments and cards operations outsourcing services, alongside offering business solutions to financial service providers in Africa and Asia. MCB Consulting Services Ltd (MCBCS) dynamically pursued its progression in line with its ‘positively disruptive’ business strategy. As key achievements, it intervened in 7 new countries and signed new partnership agreements with global players. As for International Card Processing Services (ICPS), progress was made in providing multi-channel card and payment solutions to clients located in Mauritius, the Indian Ocean, Asia and key African economies.

Beyond, we have upheld our market diversification momentum, with a key development being the launch of our new Representative Office in the Dubai International Financial Centre. In addition, while MCB Microfinance Ltd made headway in fostering the financial inclusion and empowerment of small entrepreneurs, we established the MCB Institute of Finance Ltd which aims at promoting the financial knowhow of professionals and students by way of offering in-class and online courses via renowned international partners.

Group entities have been actively reinforcing their foundations in order to be in a position to support sound and sustainable growth. While making allowance for applicable regulatory rules and compliance requirements, we strengthened our risk and capital management framework, making notable inroads in embedding a strong compliance culture throughout the organisation by means of regular training and reporting. Particular attention was also devoted to effectively handle and mitigate cyber risks, in view of their rising prominence, with further reinforcement of our relative processes and investment in more robust technological infrastructure.

In line with our already well established philosophy, we have continued to upgrade our technological platforms and have kept our business processes under constant review with a view to improving cutomer relationships and efficiency, while building the capacity to be in a position to offer our clients new products which are adapted to their ever evolving needs. Some of our major business units, like Treasury and Private Banking and Wealth Management, have undergone major transformation programmes aimed at enabling the Group to take due advantage of the positioning of Mauritius as an International Financial Centre and pursue its business development endeavours on the regional scene.

Our Digital Transformation Programme, which was initiated last year, is gaining momentum and is being scaled up to formulate innovative customer journeys, alongside contributing to improve our operational efficiency levels, enhance the quality of customer interactions and sharpen our competitive edge across dedicated segments. We made good progress in implementing an agile way of working at the level of MCB Ltd and we have set up a Change Management Office to provide the necessary structure to facilitate the implementation of ongoing initiatives. Also, we have established a Data Office to help enhance the quality and accessibility of the data infrastructure in support of our strategic thinking process, while our Customer Lab contributes towards research, encourages co-creation with customers and develops innovative solutions.

We remain committed to providing

our employees with the right skills

and competencies to perform to the

best of their abilities …

Via our HR Transformation Programme, we aim to implement world-class practices and processes to attract, develop and retain our employees, with due emphasis laid on talent management, our leadership brand and strategic talent acquisition. While setting the necessary building blocks to gear up our workforce capabilities, we remain committed to providing our employees with the right skills and competencies to perform to the best of their abilities via tailored learning opportunities. A key endeavour is to further their professional advancement and resilience towards adapting to the fast-changing and increasingly competitive environment.

As a major player within the local economy and our region, we are conscious of the key role we can play in living and promoting sustainable behaviour. Towards the end of last year, we launched our Corporate Sustainability Programme: ‘Success Beyond Numbers’. This programme centres around three main pillars namely the development of a vibrant and sustainable local economy, the protection of the natural environment and promotion of our culture as well as the welfare of the society and its people. A number of initiatives have already been launched, including our ‘Lokal is Beautiful’ campaign aimed at local SMEs, and a comprehensive programme is currently being developed. Initial reaction to the programme from our staff has been very positive and has generated a very encouraging level of participation from them. It is hoped that we will be able to also rally our clients to this noble cause.

While the global landscape remains testing, the economic conditions across countries where the Group is involved warrant close attention, although interesting growth avenues subsist in niche segments across the African continent. Group entities remain confronted by stiff competitive pressures across specific markets, partly linked to the advent of new technologies. Indeed, the increasing prominence and dissemination of digitalisation practices across industries is contributing to reimagine the way we conduct our operations and reshape the customer relationship model. In the same vein, we are being exposed to a digitally-savvy young population, with the Group called upon to provide adapted solutions to meet the needs and aspirations of its customers and employees. Mindful of the dynamic context, we will maintain our disciplined approach to the execution of our strategic plans on the back of reinforced capabilities. We will continue to focus on the strengthening of our domestic position, on expanding our non-bank activities and on growing our international footprint, with the African continent remaining a key focus area.

To pursue our expansion endeavours, we will enrich our value proposition and provide increasingly connected experiences to our customers while ensuring continuous reinforcement of our risk management, internal control and compliance frameworks. We will remain focused on implementing our three ongoing major initiatives namely our Digital Transformation Programme, the HR Transformation Programme and the Corporate Sustainability Programme.

As a major player within the local

economy and our region, we are

conscious of the key role we can play

in living and promoting sustainable

behaviour.

Against this backdrop and in line with the pipeline of opportunities at hand, we expect Group results to improve further in the coming financial year, albeit at a reduced pace given the strong performance achieved this year.

I would like to thank our valued customers for partnering with us and I acknowledge the unwavering trust of our shareholders in our ability to create sustainable value for them. Furthermore, I would like to thank the members of the various Boards of the Group for their valued insights, guidance and oversight to help the organisation to move forward and achieve its targets. On this front, I cannot but have a special thought for Gerard Hardy, our former Chairman, who passed away in March last. During the 14 years that he spent on the Boards of various companies within the MCB Group he provided us with the necessary strategic guidance and direction to steer the Group forward. Notably, he has in FY 2013/14, played an instrumental role in overseeing the smooth restructuring of our organisation, becoming the first Chairman of MCB Group Ltd.

Our strong set of results would not have been possible without the support and dedication of our staff and of the Management teams of all Group entities. I wish to thank them for contributing to making things happen and meeting our set objectives.

Pierre Guy NOEL

Chief Executive

Introduction

Our positioning in FY 2018/19

The Group faced a dynamic and challenging context across the segments and geographies in which it operates. Against this backdrop, we took appropriate strategic decisions that helped us achieve sound and balanced growth across entities.

Our underlying thinking and approach

Integrated thinking is entrenched in the conduct of our business activities and our value creation process. We design, formulate and recalibrate our strategic objectives and intents after making an informed and holistic assessment of the multiple shifts taking place across the environments in which we operate, both locally and abroad. We ensure that our business development moves and initiatives are in alignment with our contemplated strategic trajectories. Overall, this consistent and committed approach allows us to pursue our business growth in a healthy and predictable way, while setting the stage for the timely and effective realisation of our targets and ambitions.

The operating context

Macroeconomic environment

Key economic indicators

Implications for our strategy and business activities

- Amidst the generally demanding context, the Group has adopted a thoughtful growth agenda, while reinforcing its market vigilance in order to adequately appraise and respond to the needs and expectations of its individual and corporate customers.

- Alongside further diversifying business activities across markets and regions, the Group has tapped into growth opportunities prevalent across niche segments and areas where it displays strategic competencies, after capitalising on its adapted value proposition.

Market environment

Recent trends and developments

- Notwithstanding the challenging landscape, the banking and financial systems in Mauritius and our foreign presence countries have been characterised by healthy financial soundness metrics during the last financial year. The authorities remained particularly intent on modernising the monetary policy set-up, foreign exchange operations framework and payments system.

- Demand for credit has maintained an appreciable growth trajectory in Mauritius and our foreign presence countries, although moving at a relatively different pace. As for asset quality levels prevailing within the banking industries pertaining to the Group’s presence countries, they have continued to be subject to pressures, albeit improving in Seychelles.

- In spite of remedial measures taken by the Bank of Mauritius via conduct of open market operations, relatively high liquidity levels have prevailed in the banking system in Mauritius. After having edged up for some time, yields on short-term securities have witnessed a relative decline in recent months amidst the persistence of imbalances within the money market. It can be added that high liquidity conditions have also warranted attention in our foreign presence countries.

- Of interest to both the banking and non-banking entities of the Group, competitive pressures remained relatively high in some markets. In Mauritius, such challenges subsisted mainly in the mortgage and cards segments, while operators enriched their digital and wealth management solutions. Banks also pursued their regional diversification strategies. Of significance also, the Bank of Mauritius has, as from 1 August 2019, offered Silver Savings Bonds and Silver Retirement Bonds for sale to enable the elderly improve return on savings and encourage savings towards retirement.

- Generally accommodative monetary policy conditions have been upheld in our other presence countries amidst easing inflationary pressures and mixed economic conditions. In Mauritius, the Bank of Mauritius has, in August last, cut the Key Repo Rate by 15 basis points to 3.35%, after making allowance for the worsening global economic outlook.

Key banking sector metrics

Implications for our strategy and business activities

- The organisation has adopted dedicated moves to respond to the exigent market and competitive environments. It pursued judicious assetliability management, unlocked opportunities for innovation, bolstered its competitive edge and diversified its positioning across segments. In particular, it has further improved its value proposition, while entrenching the latter on a customer-centric approach.

Legal and regulatory environment

Recent trends and developments

- The legal and regulatory environment facing the Group remains dynamic and is becoming increasingly demanding.

- Amongst key stipulations of interest to MCB: (i) the Guideline for the write-off of non-performing assets was revised to provide for a broad framework and specific requirements for the write-off process at financial institutions to ensure consistency and prudence across the exercise; and (ii) the Guideline on Credit Impairment Measurement and Income Recognition was amended to align prudential requirements pertaining to asset classification and provisioning requirements with advocated provisions of IFRS 9.

- To consolidate oversight of banking players and while gradually moving away from the current compliance-based set-up, the BoM embarked on the adoption of a full-fledged risk-based supervisory framework. It includes a specific module on Money Laundering/Fighting against Terrorism risks, which reflects the increasing emphasis being laid by the authorities to tackle such risks, as it can additionally be gauged by (i) the setting up, by the Central Bank, of a dedicated unit to monitor such matters by means of off-site surveillance and on-site examinations; and (ii) the passing of the Anti-Money Laundering and Combatting the Financing of Terrorism and Proliferation Act 2019, which amended various enactments with a view to meeting relevant international standards.

- The Office of the Ombudsperson for Financial Services has recently been set up, with the body mandated to, in particular, deal with complaints received from consumers of financial services and make an award for compensation where appropriate. In the same vein, the Bank of Mauritius has proceeded with the implementation of the recommendations of the ‘Banking Your Future: Towards a Fair & Inclusive Banking Sector’ report. The declared objective of the latter is to achieve a fairer and more inclusive banking sector, with specific instructions having been issued to banks after consultations with the Mauritius Bankers Association.

- On the fiscal front, the following are worth noting: (i) for banks in operation as at 30 June 2018, the special levy – which, effective year of assessment commencing 1 July 2019, is administered under the Value Added Tax Act – has been increased from 4% to 4.5% of leviable income (i.e. net interest income and other income from banking transactions with residents only) for operators having net operating income exceeding Rs 1.2 billion; and (ii) effective year of assessment starting 1 July 2019, the relief for tax credit available to banks on foreign sourced income will no longer be available, with corporate tax rates as follows: (a) a tax rate of 5% on the first Rs 1.5 billion of chargeable income; (b) 15% for amount exceeding Rs 1.5 billion; and (c) a reduced tax rate of 5% on the amount of the current year chargeable income exceeding that of the base year if the specified conditions are met.

- The Mauritius Deposit Insurance Scheme Act was approved by Parliament and received Presidential Assent in April 2019. It aims at better protecting the interests of depositors and to guarantee the repayment of their deposits, up to Rs 300,000 per insured depositor and per member institution, in case of failure of a bank or non-bank deposit-taking institution licensed by the Central Bank. Of note, however, the legislation has not yet been proclaimed, with the BoM currently working on its operational aspects.

- With regard to our foreign presence countries, Central Banks have pursued their efforts to strengthen the regulatory oversight of operators and consolidate their respective industries. This contributed to maintain financial stability, backed notably by the emphasis laid on strengthening compliance requirements, measures to combat anti-money laundering and financial education.

Implications for our strategy and business activities

- In the light of observed developments, the Group strived to appropriately ascertain the significance of legal and regulatory stipulations for relevant entities, while proactively engaging with regulators. Entities strengthened their risk management and compliance capabilities to ensure strict adherence to mandatory rules and advocated norms, backed by reinforced processes and frameworks.

Technology and society

Recent trends and developments

- Key developments taking place on the technological front, in the advent notably of Artificial Intelligence, Big Data analytics and Blockchain technologies, are increasingly disrupting traditional business models and stakeholder relationships.

- Technological developments are calling for new strategic partnership models to be forged amongst business players, including banks and technological companies, alongside necessitating upgrades to both front and back-office operations. In Mauritius, regulators are also gearing up to keep pace with the evolving context. The BoM implemented the National Payment Switch to further modernise the relevant infrastructure for improved efficiency, safety and soundness. In the same vein, it launched the Mauritius Central Automated Switch. It is a national payment platform that operates round the clock, while setting the stage for the implementation of an Instant Payment System. As for the Financial Services Commission, it released a set of rules, which positioned the Mauritian International Financial Centre as the first jurisdiction globally to offer a regulated landscape for operators holding a Custodian Services (Digital Asset) Licence.

- In the context notably of demographic changes and the rise of the millennials, the lifestyles, behaviours, attitudes and aspirations of customers are changing at a rapid pace, with increased emphasis laid on personalised solutions and instantly accessible services. This situation is instigating heightened competitive pressures across markets segments.

Implications for our strategy and business activities

- The Group has set out to provide increasingly adapted solutions, alongside reimagining customer experiences. It further modernised information systems and digital channels, backed by the adoption of scalable, efficient and flexible platforms. It has forged meaningful collaboration and partnerships with relevant stakeholders toward contributing to the creation of impactful ecosystems.

- The Group has reinforced its data management and analytics capabilities in order to unearth organisation insights and support strategic moves. It has strengthened its risk management and internal control capabilities so as to preserve its information security and reputation, while gearing up to tackle potential cyber threats and protecting consumer data amidst all circumstances.

Positioning ourselves for growth and success

Our strategy is geared towards creating sustainable value. Anchored on our proven business model and while guiding our allocation of resources, our strategy paves the way for delivering strong earnings growth and sound financial metrics, alongside ensuring that we operate within the precinct of our risk appetite. While transforming the Group into a simpler and better organisation, we aim to deliver exceptional customer service and tap into business development opportunities locally and abroad.

Concomitantly, a key objective of the Group is to embed sustainability principles in the way we do business, alongside integrating it in our culture, values and processes, in line with our objective to be a responsible corporate citizen.

Our main strategic objectives

Our key focus areas

Our promise to creating a differentiating customer experience

To enrich customer experience at all touchpoints

To be coherent and simple in our approach

To stay innovative in our offerings

To empower customers in realising their aspirations

To simplify and streamline our operations

Our governance and processes

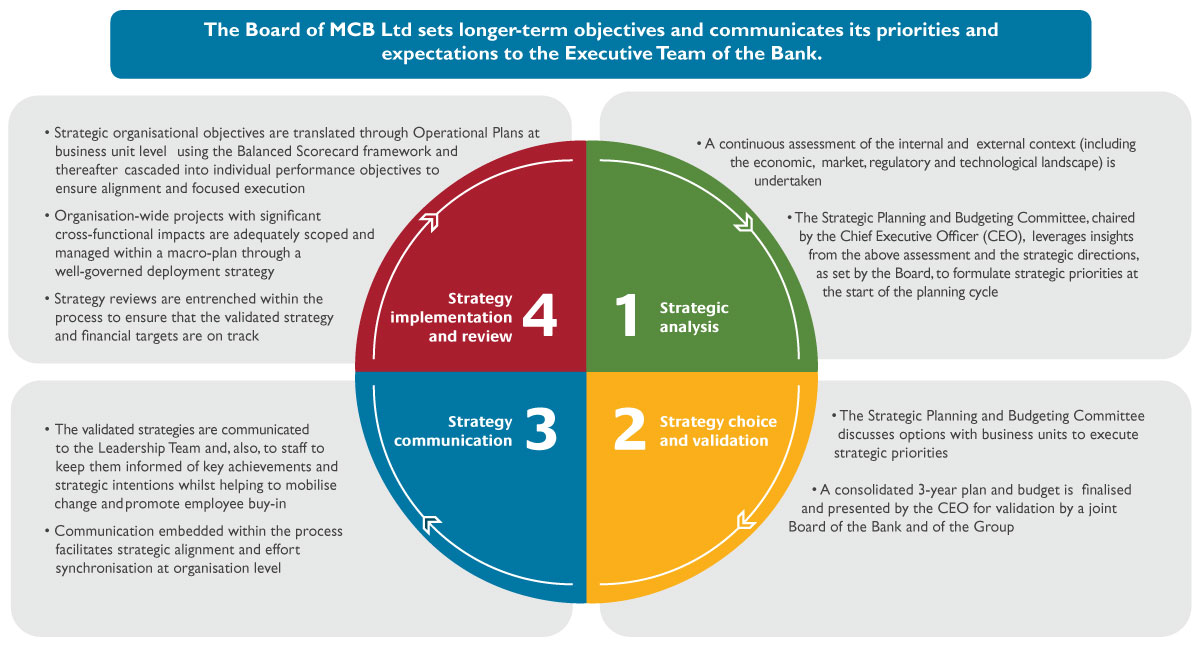

- MCB Group has a well-defined governance framework as well as coherent processes and practices to facilitate strategy elaboration, execution and review. The Board sets the strategic directions of the Group, approves strategic policies and ensures that they are communicated throughout the organisation.

- The Board is assisted by the Strategy Committee which, inter alia, makes recommendations on development strategies, assesses strategic opportunities, follows up on Group-wide initiatives and ensures that strategy execution is backed by adequate resources and structures.

- While ensuring congruence with strategic directions set at Group level, the entities formulate their own strategic orientations, which are cast in a 3-year rolling plan and endorsed by the Board at the start of each financial year.

- Alongside being subject to relevant regulatory and compliance requirements, the entities determine their strategic initiatives after taking on board the inherent specificities and exigencies of the markets in which they operate as well as the relevant challenges and opportunities characterising the businesses they pursue.

- When contemplating their strategic directions, entities make allowance for the risk appetite, as formulated across segments, while considering their capital position as well as the scale and proficiency of their physical and human resources. In their functioning, entities capitalise on Group synergies, while the services of external consultants are selectively leveraged to provide entities with competent tools and guidance in order to sustain their thinking and decision-taking process. Of note also, key priorities and performance indicators are formulated with a view to providing clarity and direction towards supporting the smooth deployment of envisioned initiatives. Entities have their own strategic planning processes. In respect of banking entities, they have a similar planning process, with the one applied by MCB Ltd depicted as follows.

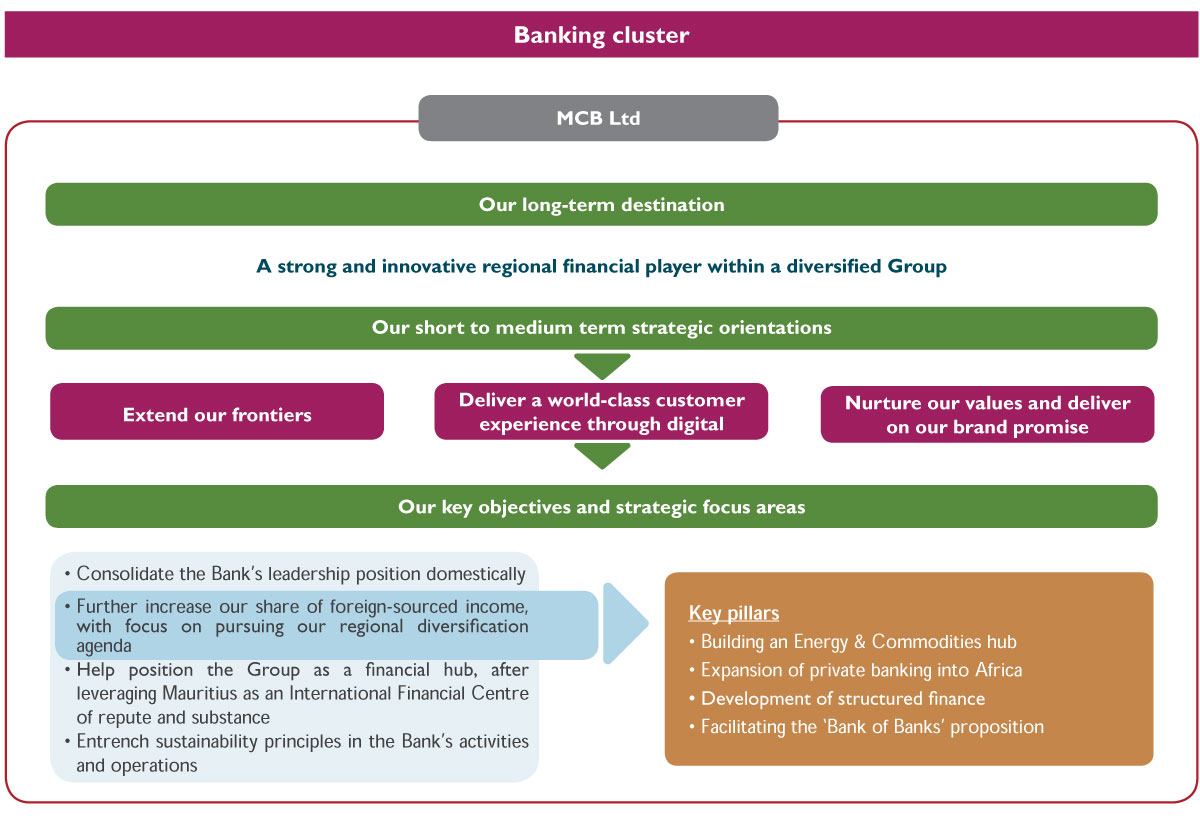

Strategic orientations and objectives across clusters and entities

Our key objectives and strategic focus areas

- Consolidate the Bank’s leadership position domestically

- Further increase our share of foreign-sourced income, with focus on pursuing our regional diversification agenda

- Help position the Group as a financial hub, after leveraging Mauritius as an International Financial Centre of repute and substance

- Entrench sustainability principles in the Bank’s activities and operations

Key pillars

- Building an Energy & Commodities hub

- Expansion of private banking into Africa

- Development of structured finance

- Facilitating the ‘Bank of Banks’ proposition

Foreign banking subsidiaries

- Increase market shares across retail and corporate segments, while positioning the entities as trusted banking partners

- Expand activities across new and emerging customer segments, with the affluent market as a key focus area, while reinforcing proximity with small and medium enterprises

- Lay greater emphasis on the adoption of digital and innovative practices, backed by the implementation of mobile banking service and upgrades to multi-channel payment platforms (e.g. Internet Banking, ATMs, POS, E-commerce)

- Improve customer experiences and widen the range of offerings to enrich the value proposition, notably relating to card solutions, retail loan facilities as well as new offerings to boost the corporate segment, notably structured financing solutions

- Leverage solutions developed by MCB Ltd in the entities’ presence countries, backed by service level agreements

- Expand physical footprint for increased market presence, while growing and modernising the branch network

‘Non-banking financial’ and ‘other investments’ clusters

- Reinforce the positioning of the Group as an integrated financial services provider locally and in the region

- Leverage the brand franchise and distribution capacity of the organisation to consolidate our positioning across long-established business areas (notably those relating to the provision of investor, factoring and leasing services), while diversifying our activities

Zoom on selected entities

- Focus on advising blue chip clients locally and arranging financing for transactions and projects in Africa

- Broaden investment management activities to alternative assets

- Invest in private equity and hybrid debt opportunities alongside partners in Africa

- Seek strategic alliances with selected partners to expand our distribution channels and strengthen our technical capabilities

- Widen the range of offerings and revamp existing products to enrich the value proposition, alongside diversifying the customer base

- Forge strategic alliances with key stakeholders, including car dealers and fleet management companies

- Maintain and nurture close relationships with business lines of MCB Ltd

- Consolidate its position in the receivables finance market by leveraging latest technological solutions and diversifying products

- Offer advisory and ‘service-only’ solutions that are customised to domestic and international businesses

- Enhance synergies with MCB Ltd to offer best-fit solutions to clients

- Consolidate the democratisation of access to credit by micro-entrepreneurs and promote financial inclusion

- Foster economic empowerment of micro-businesses and contribute to sustainable development

Develop and invest in a diversified portfolio of prime real assets with a view to seeding property yield funds to be offered to various customer segments

- Look at opportunities in emerging markets and diversify country positioning

- Deploy initiatives in respect of client experience by means of dedicated relationship management, the provision of customised and scalable payment solutions, the development of human capital, and the streamlining of our operations

- Provide solutions to wider customer base (e.g. MasterCard and Visa (EMV) issuing and acquiring, transaction processing, EMV debit, credit, corporate and prepaid card issuance, Card personalisation bureau service, ATM/POS driving, mobile payment solution)

- Expand our reach in Africa and Asia by capitalising on our position as a recognised and trusted partner in delivering payment solutions to banks and financial institutions and tapping into synergies with Group entities which are involved on the African and Asian continents

- Become a preferred and trusted business enabler, while positioning itself as leader across earmarked spheres of activity

- Consolidate footprint in existing markets and probe into new territories, notably in Asia-Pacific region

- Strengthen partnerships with and operational assistance to financial institutions, particularly in Africa

- Further exploit the potential of existing services and launch new ones (e.g. analytics and business process re-engineering)

- Nurture collaboration with relevant stakeholders in order to more effectively support business growth, while implementing the necessary frameworks and processes to monitor the performance of sealed agreements

- Increase market visibility

Creating value in a sustainable way for the benefit of our stakeholders

Our key foundations

Our proactive stakeholder engagement model informs and guides our actions and behaviours. While embracing an integrated vision that aims at providing a solid contribution to the advancement and prosperity of the Mauritian society and economy, we seek to consistently make sense of and respond to the needs and expectations of our multiple stakeholders.

Read more in Sustainability Report

Read more in Sustainability Report

The Group has a well-established governance and operational framework to ensure that engagement with stakeholders is managed in a transparent and impactful way, in alignment with international practices and regulatory stipulations. Stakeholders are kept informed about the Group’s business and strategy on a regular basis through various channels. Their views and concerns, notably gathered through ongoing dialogues, meetings and surveys, are considered in the Group’s decisions, with material issues escalated to the Board. The organisation’s activities underlying its stakeholder value creation are anchored on sound foundations. The employees of MCB Ltd abide by the Bank’s Code of Conduct and the National Code of Banking Practice. Reflecting its commitment to entrench applicable principles in its strategy and operations, MCB Ltd is an adherent to the United Nations Global Compact at participant level. The latter is the world’s largest voluntary corporate responsibility initiative for businesses committed to aligning their operations and strategies with universally accepted principles in the areas of human rights, labour, environment and anti-corruption. Since August last, MCB Ltd is one of the founding signatories of the Principles for Responsible Banking of the United Nations Environment Programme – Finance Initiative. The Principles provide the banking industry with a single framework that embeds sustainability at the strategic, portfolio and transactional levels across business areas, thus assisting operators in playing a leading role in achieving society’s goals. MCB Group Ltd is one of the constituents of the sustainability index of the Stock Exchange of Mauritius which tracks the market price-performance of listed companies that demonstrate strong sustainability practices.

Our Corporate Sustainability Programme

After leveraging the services of a renowned international consultant and conducting a series of internal discussions and envisioning exercises, the organisation designed an ambitious Corporate Sustainability Programme. While initiatives are ongoing to underpin the optimal structuring and execution thereof, the programme presently acts as our strategic anchor-point for unleashing concrete actions across key pillars towards entrenching our socio-economic involvement. The programme reflects our engagement to create sustainable value to our stakeholders as well as make the country a better and healthier place to live in. Our thoughts and initiatives are being spearheaded by crossorganisational efforts, with strategic partnerships also secured with external stakeholders so as to foster the creation of impactful ecosystems. In addition to the design of a manifesto to epitomise the Group’s renewed engagement, the ‘Success Beyond Numbers’ statement was embraced so as to reflect the vision and philosophy guiding our endeavours.

Our Corporate Sustainability Programme

Our Philosophy

Success Beyond Numbers

Our holistic investment towards making Mauritius prosper

Pillars

The development of a vibrant and sustainable local economy

The protection and valorisation of our cultural and environmental heritage

The promotion of individual and collective well-being

Key stakeholders directly and indirectly impacted

Key enablers supporting the operationalisation of the programme

- Governance framework underpinning the overall oversight of the programme

- Operational set-up defining the relevant roles, responsibilities, mandates and accountabilities

- Framework to guide the planning, execution, coordination and management of relevant projects and initiatives

- Roadmap for the timely approval and launch of projects and initiatives

- Structure in place for benefits tracking, monitoring and reporting

Our strategic achievements and initiatives

Fostering our stakeholder engagement

-

Shareholders and investors

- We upheld the image and reputation of the Group as a strategically important player. Backed by further market diversification, enhanced customer service quality and solid risk management, the Group posted a strong growth of around 31% in net profit during the last financial year. Against this backdrop, we continued to generate comfortable earnings to reward our shareholders and investors, while delivering adequate dividends and maintaining attractive returns on investment.

- The Group promoted open communication with its shareholders in order to foster strong and transparent relationships with them. As a key priority, we fostered the availability of timely, concise and detailed information on the positioning and performance of the Group. Furthermore, we regularly engaged with shareholders to better understand their perspectives.

- We continued to hold open, constructive and regular dialogues with international rating agencies with a view to reporting on the performance and prospects of the Bank as well as its strategic orientations. Along the way, we shared dedicated analyses to provide comfort as regard our risk management and business growth foundations. The year under review saw the upgrade, by Moody’s Investors Service, of the credit rating of MCB Ltd, thus further reinforcing its investment-grade profile.

- The Bank has successfully accessed global financial markets. This can, notably, be gauged by the raising of USD 800 million Dual Tranche Syndicated Term Loan Facility on international markets, which attracted significant market interest.

- We upheld the image and reputation of the Group as a strategically important player. Backed by further market diversification, enhanced customer service quality and solid risk management, the Group posted a strong growth of around 31% in net profit during the last financial year. Against this backdrop, we continued to generate comfortable earnings to reward our shareholders and investors, while delivering adequate dividends and maintaining attractive returns on investment.

-

Customers

- Backed by a thorough understanding of exigencies and requirements across market segments, we provided clients with increasingly simplified and personalised financial solutions to help them meet their goals, thus contributing to their prosperity and financial well-being. We made further headway in building life-long relationships with clients, while accompanying them in good and bad times. We pursued the digitalisation of our operations and services, alongside improving the reach and appeal of our wide-ranging channels to allow customers undertake payments and transactions in an easier, faster and safer way.

- We continued to adopt appropriate and carefully-designed communication and reporting channels vis-à-vis our customers to provide them with transparent and timely advice and information about our offerings and effectively attend to their queries. We regularly sought customer feedback on our solutions, notably via surveys and focus group discussions, towards improving our value proposition. We embraced dedicated initiatives to address customer complaints in an efficient and opportune manner. It is worth noting that 85% of customer complaints registered during FY 2018/19 have been resolved within less than 5 days as per estimates, which represents an improvement of five percentage points relative to the preceding year’s outcome.

- We preserved the security and confidentiality of transactions, alongside upholding customers’ trust in the organisation. Towards this end, we reinforced our internal platforms and processes, including our cyber risk management framework, to ensure the safety of our customers’ information, while ensuring that they can use our channels in a dependable way.

- We have strengthened client relationships and our market visibility, mainly through the organisation of and participation in various promotional and commercial initiatives, as well as international seminars, conferences and roadshows. Such events enabled the Group to promote its capabilities and value proposition, while gaining insights on international business trends and dynamics. The Group reinforced linkages with carefully-chosen business operators and other stakeholders across the market place. We remained active on social media platforms such as Facebook, Twitter, YouTube, Instagram, and LinkedIn.

- Backed by a thorough understanding of exigencies and requirements across market segments, we provided clients with increasingly simplified and personalised financial solutions to help them meet their goals, thus contributing to their prosperity and financial well-being. We made further headway in building life-long relationships with clients, while accompanying them in good and bad times. We pursued the digitalisation of our operations and services, alongside improving the reach and appeal of our wide-ranging channels to allow customers undertake payments and transactions in an easier, faster and safer way.

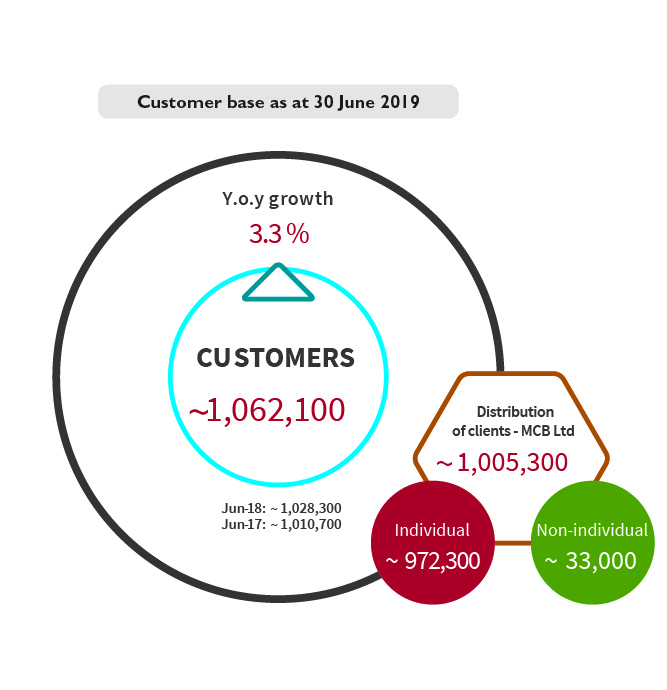

Serving a strong and diversified customer base, while leveraging innovative channels

Organisation of and participation in key events

The Group is organising the 10th edition of its ‘Africa Forward Together’ seminar in October 2019. Of note, last year’s event welcomed 24 banks and financial institutions from 11 African countries. This annual seminar offered bankers a privileged platform to network with industry leaders as well as share experiences and views on trends and business developments shaping the financial services on the continent. MCB provided its African institutional partners with avenues for forging or strengthening business relationships and leveraging collaboration opportunities.

The organisation has, for the fifth consecutive year, been the Diamond Sponsor of the Africa CEO Forum, which was held in Kigali in March 2019. The Forum brought together some 700 Chief Executive Officers from around 70 countries and spanning a wide range of industries as well as over 100 Government officials and heads of development institutions. It serves as a platform for constructive dialogue to shape Africa’s future and identify business opportunities on the continent.

To stimulate creativity, generate innovative ideas and foster enhanced collaboration with local entrepreneurs and FinTech start-ups, MCB organised the second edition of its ‘InovApp Challenge’ in March 2019, in partnership with IBM, Oracle Cloud and the Mauritius Software Craftsmanship Community. In addition to a competition organised amongst staff, the event for the public involved 60 participants. The latter worked together in teams of three to five people, with the aim being to create an original and useful IT solution. The theme was "In view of making Mauritius a true Smart island, how would you support the local economy through digital?”

Societies and communities

- The Group has continued to foster the well-being and progress of the societies and communities in which we live and operate. In Mauritius and across other presence countries, we partnered with relevant stakeholders, such as NGOs and public sector entities, towards promoting societal well-being. We provided support in key focus areas, notably community empowerment and preservation of the natural environment, arts and culture, youth development and sports, as well as education. In respect of the latter, it can be noted that our organisation has, so far, awarded 31 scholarships to Mauritian students ranked next in line with those eligible for the State of Mauritius scholarships on the Economics side at the Higher School Certificate examinations, while 34 students from Rodrigues have been awarded scholarships under the MCB Rodrigues Scholarship, enabling them to pursue tertiary studies at the University of Mauritius.

- Our corporate social responsibility activities are channeled via the MCB Forward Foundation, which is the dedicated vehicle responsible for the efficient and effective design, implementation and management of initiatives meant to embed the Group’s engagement with the communities in which it operates. In FY 2018/19, consistent with the authorities’ requirement for companies to set up an annual CSR Fund representing 2% of their chargeable income derived during the preceding year, an aggregate amount of around Rs 109.3 million was accordingly earmarked by the Group’s local subsidiaries. In line with the Government policy that 50% of companies’ CSR contributions for projects initiated prier to January 2019 be channeled to the Mauritius Revenue Authority, Rs 54.7 million were entrusted to the MCB Forward Foundation and spent on 15 projects, of which 13 are ongoing. The entity remained actively engaged into dedicated projects for the promotion of social welfare and empowerment through multiple areas of intervention. During the last financial year, particular attention was given to the provision of decent dwelling to families of beneficiaries. For instance, 15 households under the MCB Football Academy benefited from renovated housing arrangements.

- It is worth highlighting that no political donations were made during the year under review.

- By means of our personalised solutions and thoughtful channel distribution, we promoted financial inclusion in Mauritius, thus enabling our low-income customers to get access to credit and improve their conditions. We helped individual clients achieve their ambitions, including buying a home/car or paying for personal expenses. With regard specifically to the tailored financial solutions of MCB Ltd: (i) the low minimum balance for account opening and the fact that our savings account bundle bears no cost make the offer extensively accessible; (ii) parents are invited to open Junior accounts to encourage our young generation to be financially responsible and save from a young age; and (iii) our unsecured personal loan offer, which is also available to non-MCB customers, is often sought by low-income customers to cover for education and housing purposes. Furthermore, we provided innovative and customised solutions to SMEs as well as micro-enterprises and self-employed individuals, thus benefiting business people and households.

- We made further inroads in preserving our cultural heritage, while promoting the dissemination of arts. We took the leading role in sponsoring and/or spearheading the materialisation of key projects aiming to promote local talents at various levels, including music, singing and dance, art and writing, photography, painting and sculpting, as well as theatre and performing arts. On another note, we encouraged the adoption of environmentfriendly and energy-saving practices in our operations and business activities. Since May 2012, MCB Ltd adopted the Equator Principles, which is a voluntary and internationally recognised risk management framework, espoused by many financial institutions worldwide, for determining, appraising and managing environmental and social risks in project financing. This framework stands as the foundation and guiding principle of the Bank’s Environmental and Social Policy, which articulates the principles, policies, roles and responsibilities through which the Bank ensures the environmental and social risks management of its lending activities, in particular regarding any project or undertaking entailing loans of an aggregate amount greater than or equal to USD 2 million and with maturity of at least 24 months. As a key strategic thrust, the Bank continued to monitor and assess its direct environment footprint in order to minimise the impact of its activities on the environment. The Bank remained committed to raising awareness amongst its employees and external stakeholders, while engaging with them to stimulate the adoption of sustainable habits and work towards environmental protection. We worked towards effectively managing our direct carbon footprint, driving eco-efficiency performance and greening the supply chain. For instance, the Bank seeks to ensure that all suppliers comply with sustainable procurement standards. Also, it actively promotes the use of e-statements by customers. The total number of customers subscribing thereto increased by nearly 6% during the year ended June 2019. In the same vein, in order to reduce the environmental impact of our activities and operations on the society and community, an electronic communication campaign was launched in July 2019 to encourage shareholders and bondholders to receive the soft copy of our Annual Report by email instead of the hard copy usually sent to them. A positive response was received from shareholders. Moreover, we encouraged environment-friendly and energy-saving investments, as it can particularly be gauged by the provision of the third edition of our preferential credit facilities termed as ‘Green loans’ (see pages 63 and 72 for more details).

Authorities and economic agents

- We assisted our presence countries in their endeavours to promote the development and modernisation of their respective economic sectors and financial jurisdictions. In Mauritius, alongside financing key projects shaping the economic landscape, the Bank helped to foster the sustained growth of the country’s businesses. We have remained a dedicated and trusted partner for large corporates and investors, while upholding our commitment to accompany small and medium enterprises across a broad range of economic sectors by means of our tailored and modular solutions. Furthermore, the Bank helped to position the Mauritian jurisdiction as an International Financial Centre of substance and good repute, backed by support provided to businesses transiting through our country to conduct business across the African continent.

Helping the economies where we are involved to prosper

Direct contribution of MCB Ltd to the Mauritian economy (FY 2018/19)

Contribution to value added

~ 4%

~ 55%

Creating jobs on the nationwide scale

~ 20%

~35%

Paying taxes in support of Government revenue mobilisation

~10%

Notes:

(a) Total corporate tax paid Includes levies charged on income

(b) It excludes our indirect contribution induced by tax paid by our suppliers

~50%

Direct contribution of MCB Seychelles to the Seychellois economy (year 2018)

~1.5%

~25%

~11%

Note:

Figures displayed above are indicative, based on officially-reported data and MCB staff estimates. Furthermore, they depict the direct contribution of the entities to their respective economies, after leveraging official methodologies and advocated international norms. As such, they do not make allowance for the indirect impact of their operations and banking activities. In our Sustainability Report, an analysis of the latter impact at the level of MCB Ltd has been carried out by our international consultant, namely Utopies. As per estimates by the latter, the overall direct and indirect contribution of MCB Ltd to the country’s GDP amounted to 17% during the year 2018.

- We safeguarded the perennity and soundness of our operations, alongside fully coping with specificities and implications of evolving mandatory provisions and requirements. We ensured strict compliance with relevant regulatory limits and guidelines relating notably to business operations, product development, market development and risk management in the jurisdictions within which we operate. We assisted in strengthening the regulatory framework on the basis of our close collaboration with the regulators. We attended to regulatory reviews with notable attention to detail and professionalism, while promptly reacting to matters raised. We submitted reports in a timely manner to regulatory bodies, while transparent relationships were forged to promote adequate monitoring of our activities and informed discussions about relevant issues.

Employees

- As key endeavours during the last financial year towards embedding our position as an employer of choice, we pursued our efforts to attract, develop and retain talents as well as empower them to deliver their best, alongside further developing and leveraging the collective skills, knowledge and experience of our staff. Concomitantly, the Group engaged with staff at different levels to adequately understand and respond to their needs. On a more holistic note and as a major undertaking for the period, the Group has pursued the implementation of its HR Transformation Programme (see page 66). The aim is to reinforce human resource frameworks and processes, in support of enhanced performance deliveries and business growth.

- The subject matters to which the Group is exposed to are getting more complex and client solutions increasingly sophisticated. Against this backdrop and backed by a forward-looking approach, we remained intent on bringing about relevant upgrades to our learning framework and culture. Overall, dedicated programmes to step up the quality of our human capital include the conduct of training courses and lectures held by international experts at our Learning and Development Centre. Employees benefit from technical training as well as courses meant to develop soft skills, either delivered in-class or on-line. Worth noting, our range of courses has lately been enriched with those provided by the MCB Institute of Finance.

- Capitalising on its fair and robust remuneration philosophy, the Group strived to reward its employees adequately, in line with market conditions and meritocracy principles. Also, the Group provides a range of fringe benefits to its employees to help them in their personal life. In addition to that, our employee share option scheme (see page 108) provides eligible employees with the opportunity to partake in the growth and prosperity of the Group, through acquisition of its shares.

- The Group continued to work towards entrenching a balanced and diversified workforce in terms of gender, age group and experience in order to tap into a wide range of knowledge, skills and specialist competencies in view of creating the right conditions to achieve business strategies. In addition, the Group maintained a stimulating work context by fostering secured and healthy environments. While being compliant to legal and regulatory requirements, the Occupational Safety and Health Policy of MCB Ltd aims to foster a sound working environment and system of work for the benefit of its employees, as far as it is reasonable. Moreover, the Bank further deployed programmes to uphold the overall well-being of its employees. In addition to dedicated wellness initiatives, the Bank further implemented its Flexible Working Arrangement (FWA) initiative to support its staff. Lately, this was enriched with the ‘Work from Home’ arrangement, initiated on a pilot basis. The arrangement aims to help employees maintain a healthy work-life balance, while working from the comfort of their home and avoiding undue time to be spent in the traffic.

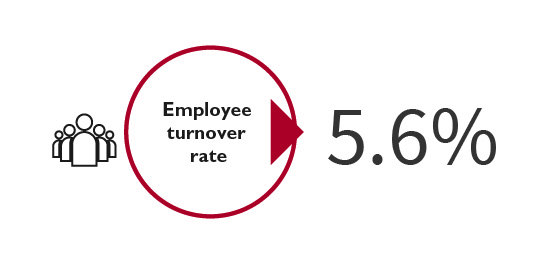

General stability of our workforce as at 30 June 2019

Notes:

(i) Retention rate is the ratio of the number of employees that stayed during a specific period to the number of employees at the beginning of the period

(ii) Turnover rate is the ratio of the number of employees that left to the average number of employees during a specific time period

Our performance across entities

Banking cluster

MCB Ltd

Financial performance

In spite of the challenging operating context prevailing in Mauritius and abroad, the Bank recorded a solid financial performance. Net profit for the year increased by nearly 30%, with the Bank’s contribution to Group results amounting to Rs 8,338 million. This outcome was underpinned by a rise of 21.2% in net interest income, which was essentially linked to the solid expansion of our loan book, notably attributable to our international activities. Non-interest income rose by 14.7% on the back principally of the continued rise in net fee and commission income, whereas ‘other income’ increased by 23.6% mainly driven by the significant fair value gains on equity instruments now included in the ‘statement of profit or loss’ following the adoption of IFRS 9. However, a subdued performance was recorded in respect of profit on exchange, reflecting unfavourable market conditions. Our cost to income ratio declined by 3.3 percentage points to attain 33.7%, in spite of operating expenses edging up by 8.6% on the back of initiatives to strengthen our human resource and digital capabilities.

Our business development

The financial performance of the Bank was supported by sustained and thoughtful efforts to execute its business expansion agenda. The Bank delivered on its strategic focus areas by strengthening its leading banking position on the local scene and pursuing its regional diversification endeavours across key growth pillars. At the same time, the Bank continued to mobilise the necessary resources to build sustainable capabilities for growth, with guiding considerations being customer focus, an engaged and agile workforce, seamless operations, an innovative culture as well as a robust risk and compliance framework. On the operational front, the Bank pursued business transformation and realignment initiatives with notable organisation-wide ramifications, aimed at supporting strategic endeavours and laying foundations for the future.

As another underpinning of its growth ambitions, the Bank successfully signed and closed a general syndication for a USD 800 million Dual Tranche Syndicated Term Loan Facility, obtained from a consortium of banks spanning Europe, Middle East and Asia. The objective is to help the Bank execute on its African ambitions, while further optimising and diversifying its funding profile.

Looking ahead, while coping with the demanding operating landscape and adopting a disciplined approach, the Bank will resolutely move forward to uphold its balanced business growth and key financial soundness metrics. Essentially, it will pursue the execution of its three-pronged strategic objectives, namely to extend its frontiers, deliver a world-class customer experience through digital, and nurture its values and deliver on its brand promise. While being currently well embarked on multiple initiatives towards building the bank of the future, we will further bolster our ability to tap into growth opportunities surfacing locally and in the region.

Delivering on our growth pillars

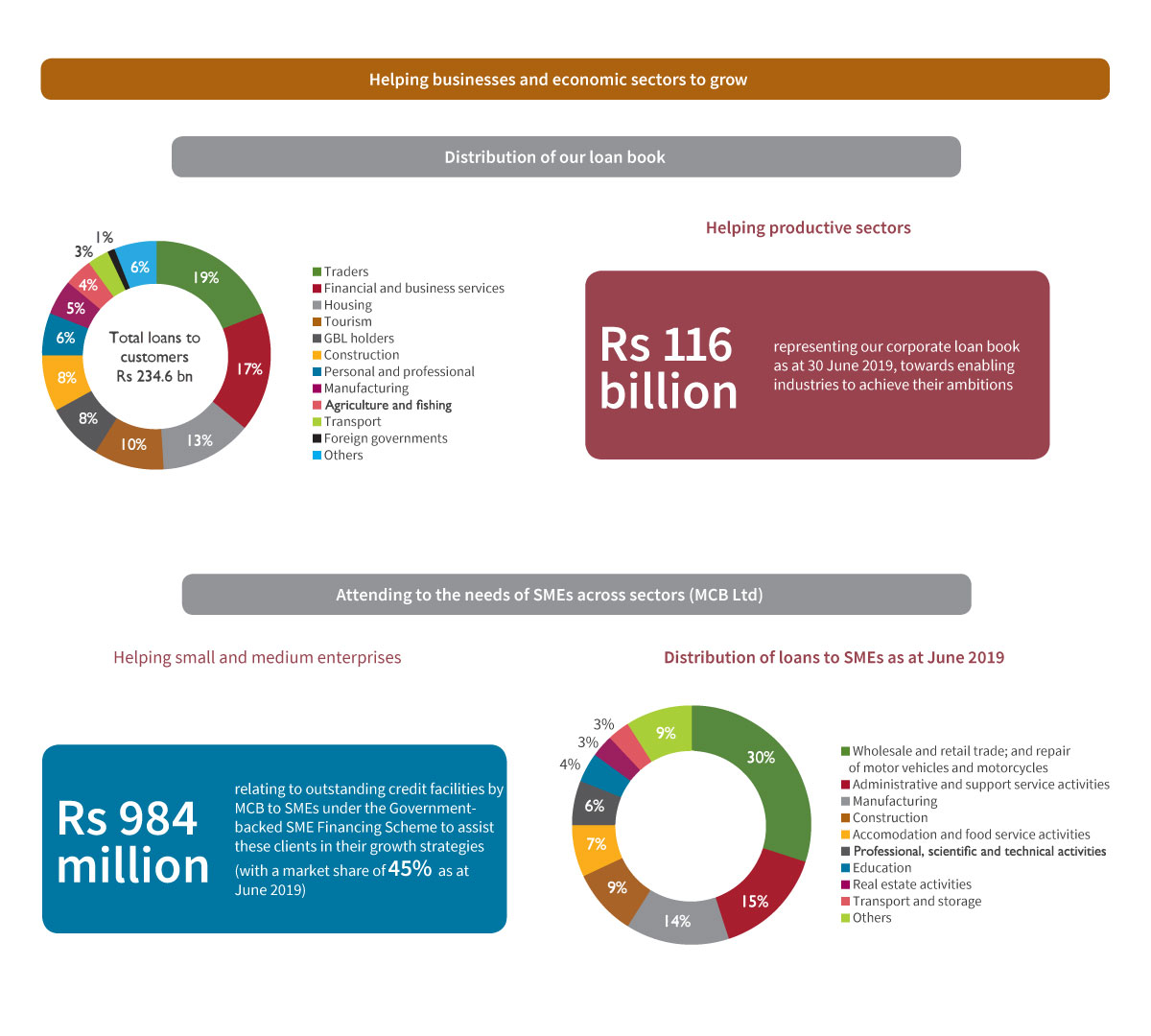

- MCB continued to adopt a disciplined and customer-centric approach to assist businesses and investors. It capitalised on (i) its unique selling propositions and tailored products and services; (ii) the reinforcement of staff capacity as well as the consolidation of tools and processes in support of improved operational excellence and risk management; (iii) the development of closer relationships across market segments; (iv) the optimisation of organisational synergies and promotion of a cross-selling culture across the Group. Reflecting our engagement, our market share in respect of domestic credit to corporates stood at around 42% as at 30 June 2019, consolidating our status as the premier business partner of companies.

- During the last financial year, we contributed to the materialisation of key projects reshaping the landscape of Mauritius. We expanded our exposures vis-à-vis customers operating across key economic sectors, particularly tourism, property development, construction, and financial and business services. We accompanied corporate and institutional clients in their growth endeavours, capacity building moves and restructuring initiatives, while acting as a trusted business advisor. Along the way, the Bank remained actively involved in the provision of ‘Green loans’, pursuant to the lending facility availed from Agence Française de Développement (AFD), in the context of the latter’s green finance label titled SUNREF (Sustainable Use of Natural Resources and Energy Finance). The key objective of the facility is to stimulate the deployment of renewable energy and energy-efficient technologies, save energy and reduce carbon emissions. In September 2018, following the success of the first two lines of credit in respect of which it had remained the most active drawer, the Bank renewed its partnership with AFD as a participating bank for the 3rd phase of the SUNREF programme in Mauritius. This new line consisted of a financial package of EUR 75 million. Our ‘Green Loans’ have been offered to a wide range of individual, SME and corporate clients in Mauritius, while we also attended to the needs of customers in some foreign presence countries. On another note, we delivered a broadening range of adapted treasury structured solutions to meet the evolving needs of our clients, alongside further disseminating our electronic forex platform, i.e. MCB Wave, which our treasurers leverage as an all-in-one digital and day-to-day tool to manage trading requirements. It is also worth highlighting that, as an authorised MUR fixed income Primary Dealer appointed by the Bank of Mauritius, the Bank was actively trading on the primary and secondary markets.

- We made further inroads in attending to the needs of companies leveraging Mauritius as an International Financial Centre (IFC) of repute and substance. In the wake of the testing operating landscape facing its customers, the Bank has maintained its thoughtful business growth agenda and broadened its involvement vis-à-vis global business entities, trusts and foundations after capitalising into the positioning of Mauritius as a gateway for conducting business with other regions. Our market development initiatives were underpinned by the delivery of adapted solutions and enhanced client interactions.

- Backed by a thorough understanding of client requirements, the Bank has cemented its positioning as the foremost service provider for SMEs in Mauritius, alongside continuously enriching its value proposition. In this respect, the organisation has, in the wake of its Digital Transformation Programme, launched a digital platform to simplify the end-to-end journey for SME Account Opening and materially improve the customer experience (see page 71). Moreover, we strengthened the SME ecosystem with the launch of the MCB Business Introducer Program in line with our engagement to empower entrepreneurs. It is a platform whereby we facilitate direct interactions of SMEs with local Accounting firms with a view to forging new business relationships. Based on their expertise, these firms help SMEs structure their business and uplift internal processes, towards better managing their day-to-day accounting needs. In the same vein and reflecting its commitment to promote responsible banking, while providing its clients of an ecosystem of services, the Bank has, in the context of its ‘Lokal is Beautiful’ proposition, introduced a dedicated scheme aimed at improving access to finance to Mauritian entrepreneurs who can demonstrate the positive impact that their activities can yield on the welfare of the society and nation (see page 72).

Patrick Beauduin

Well-known speaker, Patrick Beauduin, hosted a conference for our SME customers in July. He analysed the impacts of digital evolution on the ways in which brands communicate to their customers.

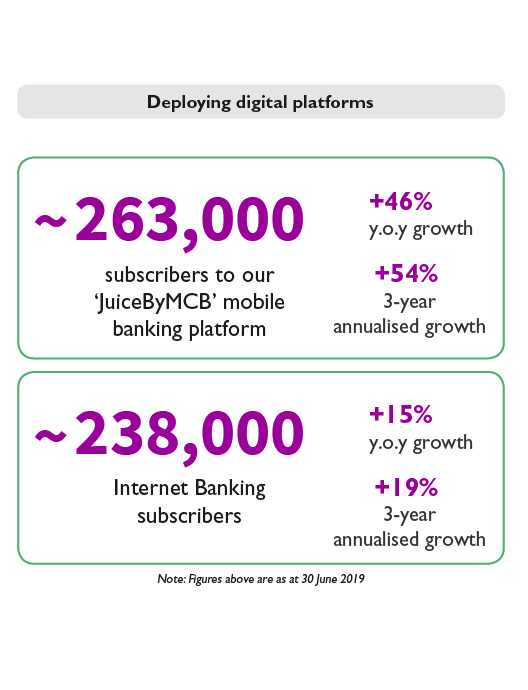

- During FY 2018/19, MCB has remained exposed to heightened competitive pressures across several segments. Yet, the Bank pursued its strategic intents and maintained its prominent market positioning across age and income groups. Alongside reflecting our strong brand, such headway was underpinned by our sound business development trajectories, strengthened operational capabilities, innovative technologies, active on-the-field presence, and continuously refined value proposition. As a key focus area, the Bank stepped up its efforts to upgrade and promote its digital channels vis-à-vis its client base. We have remained active on the payments scene by allowing clients to make and accept payments in a quick and hassle-free way via multiple channels (see page 68).

- Within the mass and mass affluent segments, in addition to strengthening our prominent footprint in respect of education loans, we have, as a key achievement, consolidated our leadership market position in mortgage. Our market share for housing loans stood at around 37% as at end-June 2019, on the back of a growth of nearly 11% in our loan book. Alongside leveraging digital channels and simplifying the end-to-end customer journey for obtaining or refinancing a housing loan (see page 71), MCB refined the appeal of its mortgage solution, which has been further customised to meet different client needs. Overall, the Bank continued to adapt and promote its tailored offerings, with a case in point being the ‘Neo Bundle’, which aims at giving customers an enriched experience through a package of products and services. Moreover, we further endeavoured to encourage our customers to save and invest. Alongside distributing the Group offerings (including notably investment solutions), we have redesigned our ‘Rupys’ savings account, which is dedicated to clients under 18 years old.

- The Bank made further progress towards meeting its objective of acting as the trusted lifetime partner for its affluent and high net worth customer base in Mauritius. Towards this end, it capitalised on its differentiating service quality and bespoke offerings, notably relating to its increasingly sophisticated range of investment and wealth management solutions. As a key offering, our customers continued to take advantage of our Lombard loan, which enables them to utilise a wide spectrum of credit products, which are secured against their existing investment portfolios. To underpin our strategic thrusts, we tapped into strengthened customer interactions and enriched offerings. Specifically, our value proposition was, during the last financial year, enhanced with the introduction of (i) a premium flexible housing loan offer, which allows for adequate flexibility for the facility repayment and contains differentiating features, including an interest rate which is aligned with the project value, the required financing and credit assessment amongst others; and (ii) a 31-Day Notice Account, which is an interest-bearing USD /EUR deposit account offering a convenient and flexible solution to customers.

- While maintaining a disciplined approach, the Bank made further progress in extending its frontiers abroad. Alongside embracing an opportunistic stance to diversify its market positioning and tap into interesting opportunities, the Bank has remained mainly involved in niche areas where it displays strategic competencies. Consequently, we have continued to deepen our relationships with existing clients and selectively extended our customer base across segments and geographies. Overall, by upholding and reinforcing the growth momentum of its businesses as well as nurturing a wide range of business partnerships, the Bank has positioned itself as a dependable and competitive banking player in Africa. To underpin its market development initiatives, the Bank has capitalised on its customised solutions, regularly-updated risk appetite, a network of some 1,150 correspondent banks worldwide (including around 200 in Africa), Representative Offices as well as the Group’s foreign presence via its subsidiaries and associates. Of note, the Bank has opened a Representative Office in the Dubai International Finance Centre in July 2019, which marks another milestone with regard to MCB’s strategy for extending its frontiers and further diversifying its revenue streams.

- We have further broadened and diversified our portfolio of international structured finance, with the Bank financing major development projects across various economic sectors (mainly power, transport, telecommunications, manufacturing and hospitality), countries and products on the African continent, while being also increasingly involved beyond. We strengthened our rapport with existing clients and built on new relationship, alongside developing key relationships with top corporates and private equity Funds in Africa. Towards these ends, we remained actively involved in delivering a comprehensive suite of adapted financing, including project financing, acquisition financing and corporate lending, while offering our products and services via bilateral lending, club deals or syndicated facilities in order to suit the specific requirements of our clients.

- We reinforced our involvement in Energy and Commodities (E&C) financing, backed by our tailored value proposition, a robust risk appetite framework, as well as strong front-to-back internal processes, with specialised and dedicated resources being recruited in a transaction management and structuring capacity. We consolidated our positioning in key markets, alongside capturing opportunistic flows in other countries, supported by the deepening of relationships with a broad range of clients. Whilst moving towards mid-sized and big traders, we consolidated the trade finance segment of our portfolio. Beyond this sphere, we prudently diversified into the African oil and gas structured debt market. We made significant progress in shifting towards medium to longer-term financing along the value chain by widening our involvement across the upstream business, alongside playing a pivotal role in securing the petroleum products requirements of some countries in Africa.

- The Bank has, in close connection with the Group, remained an active promoter of the ‘Bank of Banks’ initiative, which consists of providing a palette of adapted solutions to financial institution counterparts, notably those operating in Africa. The Group partnered with and assisted some 91 financial institutions worldwide, including over 60 in Africa and spanning 24 countries in FY 2018/19. We enabled clients to gain access to state-ofthe-art services offered by various entities, thus helping them to underpin capacity building and business growth initiatives, while accessing industry best practices.

- MCB took dedicated initiatives in view of positioning itself as a reference in the region for premium banking and wealth management expertise, in line with a key growth pillar, which is to expand private banking into Africa and beyond. In spite of being confronted by a challenging operating environment amidst unsteady financial market conditions, total assets under management increased, while our international clients edged up, with major inroads made being across Europe and Middle East. This performance was backed by our sophisticated value proposition as well as active brand and relationship-building exercises. On the marketplace, we have reinforced our status as a trusted lifetime partner vis-à-vis our client base by delivering bespoke solutions, notably those that are geared towards the safeguard, growth and transmission of customer assets. In addition, MCB set out to further position itself as a unique point of contact for serving External Asset Managers, Multifamily Offices and independent financial advisors, while offering a suite of differentiated investment and banking solutions, from transactional to multi-asset class trading.

Africa Forward Together seminar

Our Africa Forward Together seminar, bringing together C-Suite delegates and decision-makers from Africa and beyond.

Key projects underpinning our business growth agenda

HR Transformation Programme

- The organisation boarded onto this programme to gear up the quality of its human capital in order to better support its growth strategies. It aims to implement world-class practices and processes to attract, develop and support employees who are engaged in their work and are motivated to perform at their full potential. Key objectives are to (i) implement a transparent talent management framework, while growing and retaining the best talents; (ii) create a set of leadership values and develop an attractive employer brand; (iii) refine the performance management framework to foster an environment of trust, high aspiration and high achievement; (iv) foster strategic talent acquisition by determining the right moves for identifying, attracting and hiring top talent; and (v) boost operational efficiency levels via upgraded systems, processes and practices.

- Towards crafting the transformation programme, we retained the services of a world-renowned HR consulting practice. Till date, major milestones have been realised following the elaboration – through a consultative process involving key stakeholders – of a new operating model and structure for the Bank’s HR function. A strengthened Talent Management Framework has been developed to meet strategic challenges faced by the organisation, backed by enhanced partnering of the HR function with business lines and entities in support of value creation. Further headway is being realised in terms of Leadership development, underpinned by the formulation of our Leadership Brand statement and Leadership Competency Framework. Alongside ensuring that all employees are treated in a fair and equitable manner, our performance management system is being reviewed, with emphasis laid on the business context, organisation culture and integration with other human resource systems/frameworks.

Private Banking and Wealth Management Transformation Programme

- To bolster operational efficiencies and better support its growth ambitions, MCB is currently engaged in an ambitious programme aimed at reinforcing the strategic positioning of its Private Banking and Wealth Management function. Key objectives are to (i) redefine our value proposition; (ii) optimise our operating model, while bolstering inherent capabilities and building scalability; and (iii) set the foundations for the right international business culture. The Bank aspires to capture attractive business opportunities, whilst enriching the experience for its customers, employees and other stakeholders.

- To ensure feasibility and foster ownership of recommendations proposed by our international consultant, employees have been closely involved at each stage. An in-depth current state assessment has been carried out in comparison with best practices. Up to now, a new operating model and organisation chart has been approved for the Private Banking and Wealth Management function. This would notably underpin the execution of key initiatives, including the formulation of a refined client segmentation model and the crafting of business development plans towards increasing share of wallet in the local market and furthering expansion in Africa and beyond.

Treasury Realignment Programme

- Key objectives of the project are to define a medium-term strategic vision and roadmap to establish a best-in-class Treasury function at the Bank, while (i) reinforcing asset-liability management; (ii) enabling organic growth through improved Bank-wide offerings; and (iii) tapping into avenues linked to the positioning of Mauritius as an IFC and prospects across Africa.

- So far, the Bank has elaborated a new operating model for its Treasury function. It is currently in the process of finalising the formulation of an action plan for the identification of key talents and responsibilities to fulfill set mandates as well as the implementation of a change management plan amongst others.

- During the last financial year, the Bank has remained committed to embedding operational excellence and innovation as a key enabler of enriched customer service quality and relationships. The Bank further broadened its digital footprint and continued to unleash dedicated initiatives to accelerate the migration of customers from branches to digital channels. This contributed to further enhance the speed and flexibility with which we deliver value to customers. Specific moves have been pursued to ensure that customer needs are fulfilled in a fast, accurate and simple manner.

Pursuing our Digital Transformation Programme

- MCB has been engaged in building human and technological capabilities to execute an ambitious roadmap of initiatives that would cater for the full-fledged execution of its Digital Transformation Programme. Alongside achieving more agile and productive operations and strengthening the Bank’s competitive edge, a key ambition of MCB is to deliver a more convenient and appealing experience to clients, insofar they are, themselves, becoming increasingly ‘digital’ in their behaviours. The success of our Digital Transformation programme was highlighted by a survey by McKinsey. It showed that MCB’s Digital Quotient – which is a measure of our digital maturity across the areas of strategy, culture, organisation and capabilities – improved by 30% over the year to attain a score of 43 in April 2019, which is significantly above the banking peer average score of 34.