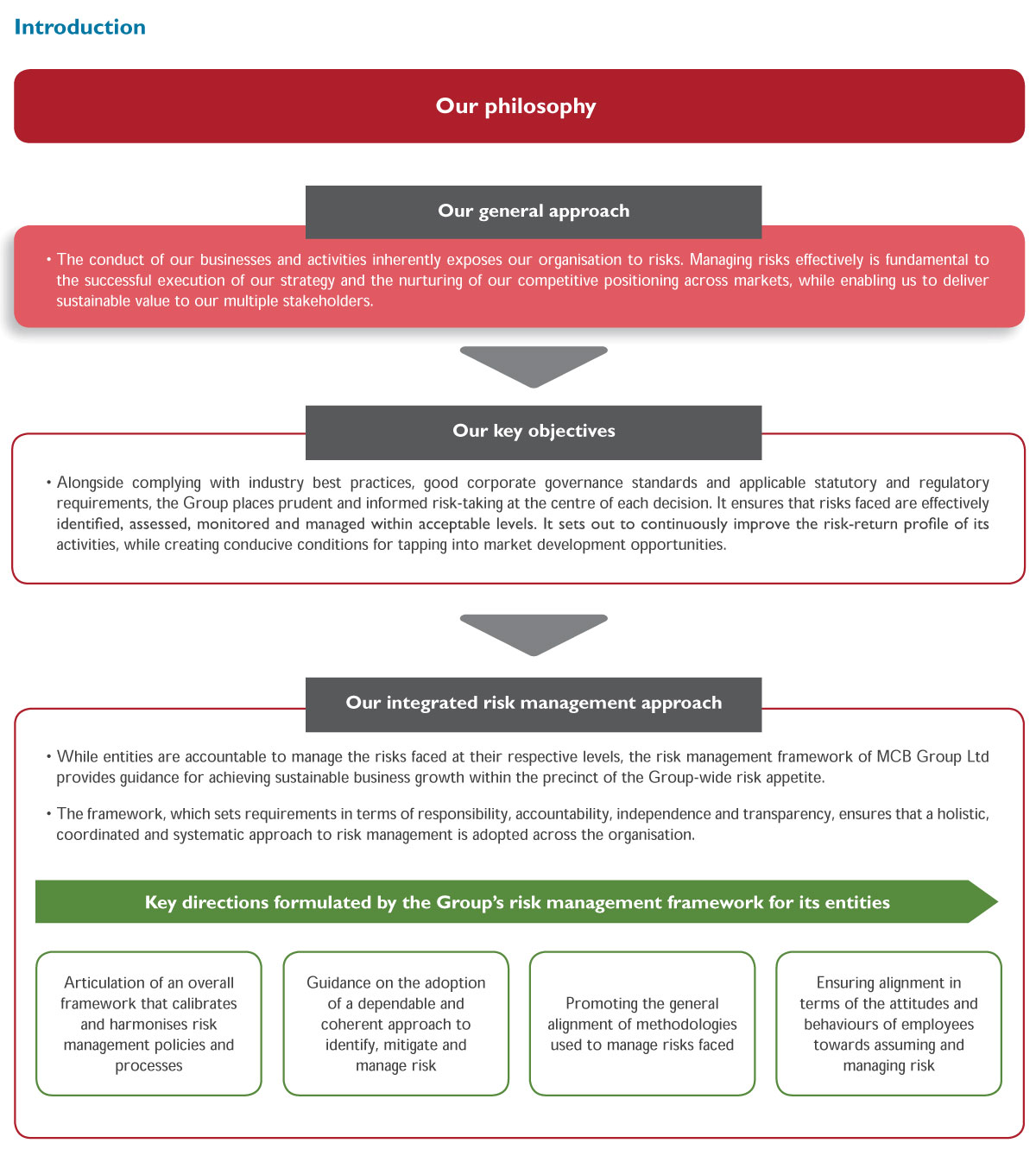

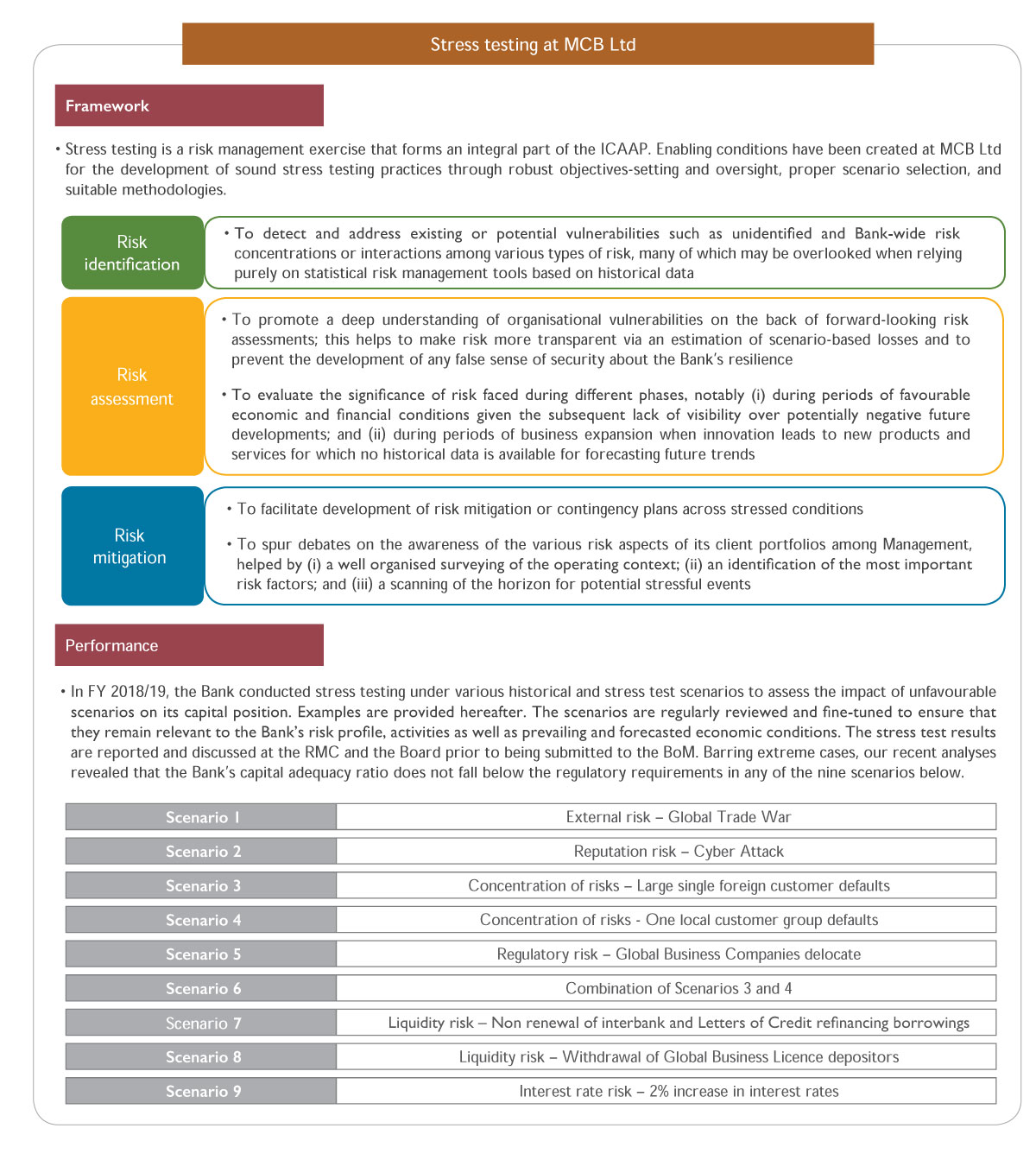

Risk And Capital Management

Foundations and focus areas

- Ensuring that our risk management principles are anchored on advocated industry norms and good corporate governance principles

- Adherence by entities to sound capitalisation, asset/exposure quality and funding/liquidity management principles

- Establishment of strong governance frameworks, with clearly-defined and segregated authorities, accountabilities and responsibilities taking

for on and managing risk - Establishment of clear risk appetite which sets out the types and levels of risk that the Group is willing to take

- Availing strong, coherent and harmonised risk management processes, policies, limits and targets

- Catering for an adequate balance between risk and reward considerations

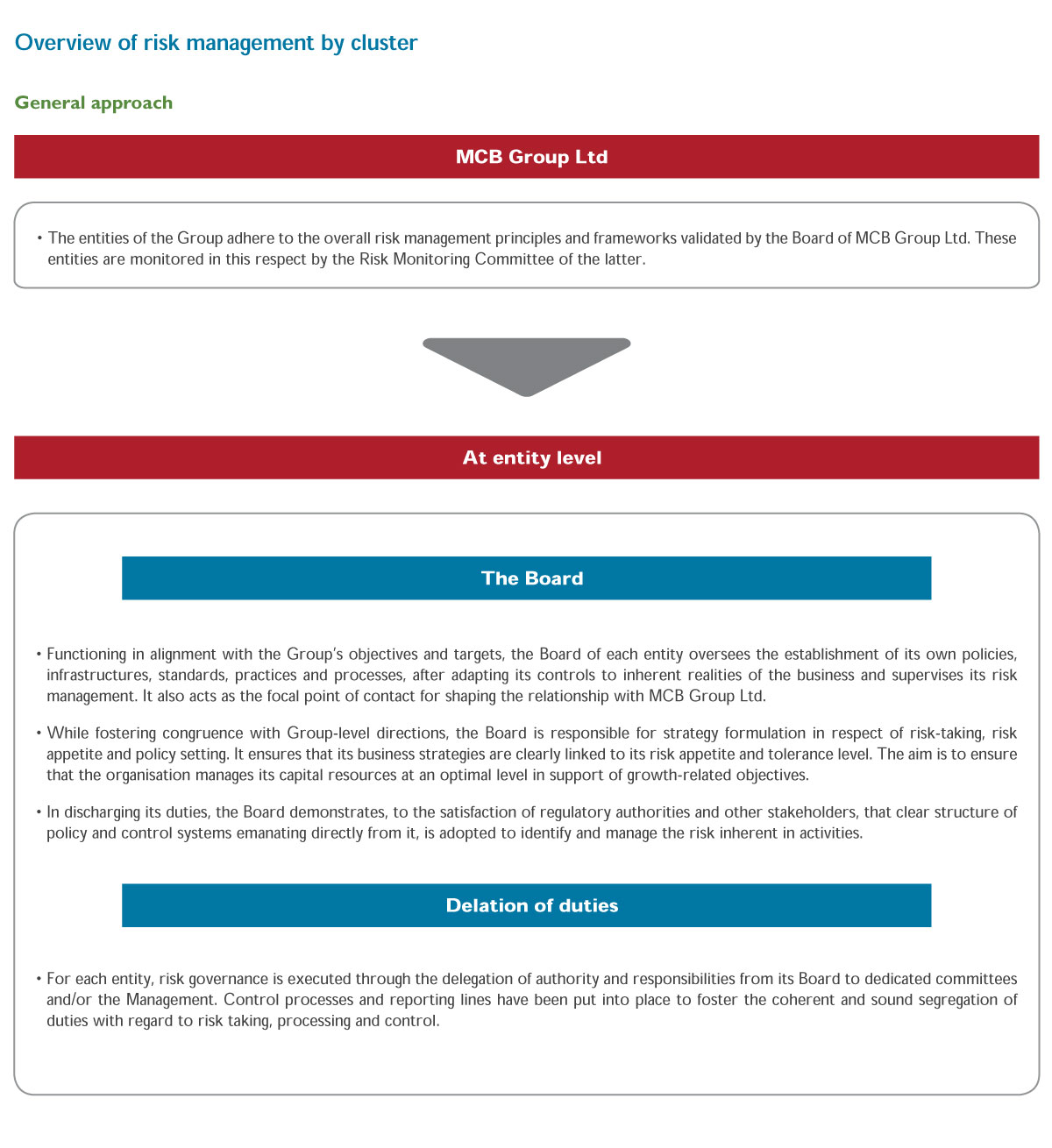

- Ultimate responsibility of the Board of MCB Group Ltd for risk management, with responsibilities delegated to its sub-committees

- Direct oversight exercised by the Boards of entities and their relevant committees

- Effective delegation of authority from the Board of each entity to its management and risk functions, with the scoping of the latter

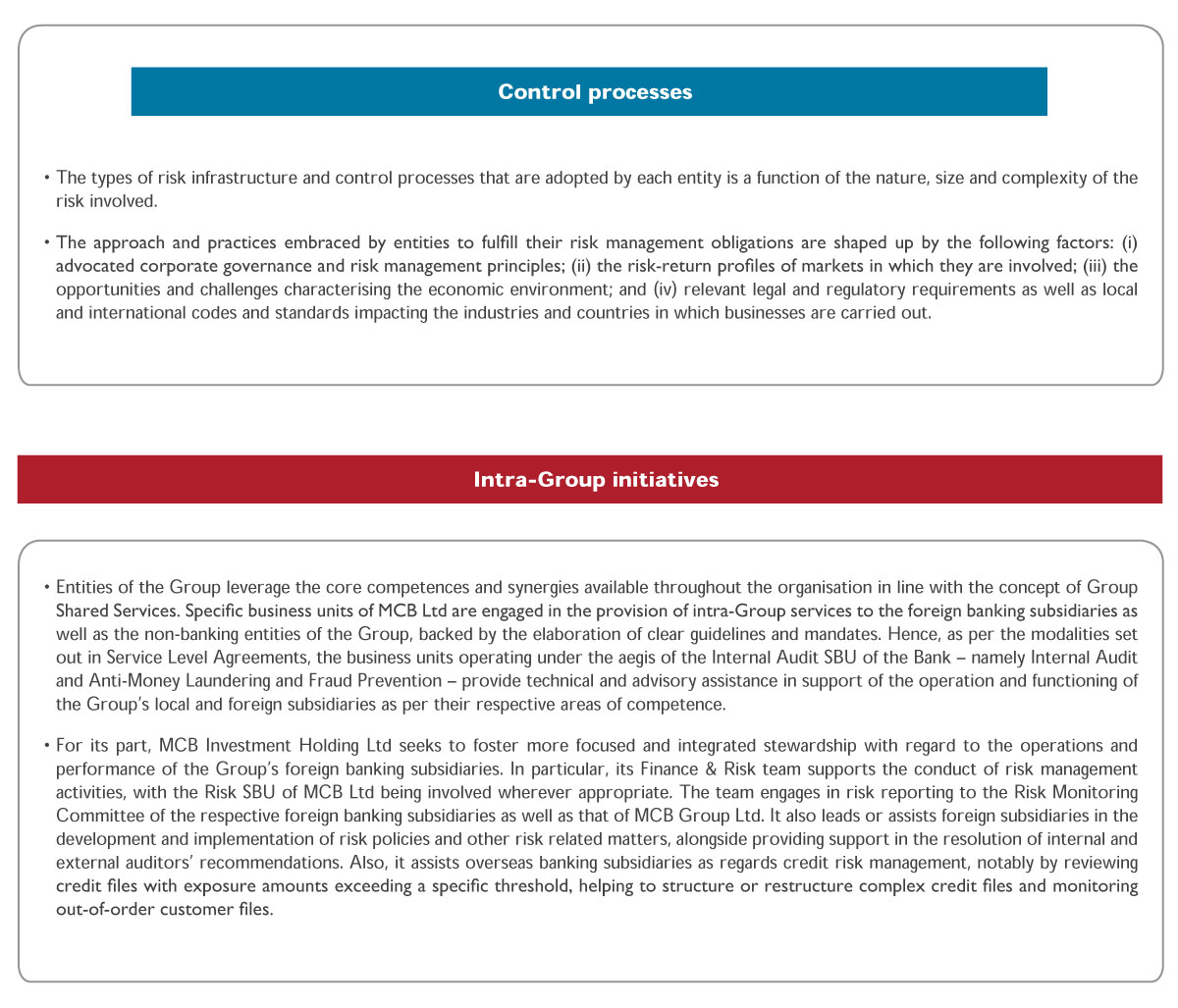

depending on the nature and depth of relevant operations and activities - Well-defined intra-Group service delivery and collaboration in support of effective risk management, as gauged by MCB Ltd providing

inter alia internal audit and compliance services to other entities where appropriate

- Regular review and update of risk management practices to ensure consistency with business activities and relevance to financial strategies,

while catering for changes in the economic and market landscapes - Adoption of policies and processes that are clear and simple to be understood and executed, alongside ensuring that they are welldocumented

and disseminated across all layers of the Group - Adherence to a common set of behaviours, attitudes, skills and guiding courses of action that are integrated throughout the Group in support

of coherent decision-taking at all levels of the organisation - Ensuring that the price charged for solutions is reasonable in relation to the relative riskiness of the exposure

Positioning and performance of the Group

Key initiatives and achievements during the last financial year and until recently

-

General moves

- In FY 2018/19, the entities of the Group upheld their healthy business development and preserved their financial soundness, while diversifying portfolios across segments and geographies. Against this backdrop and as a major achievement, Moody’s Investors Service has upgraded the credit rating of MCB Ltd in July last, with our long-term deposit rating improving from Baa3 to Baa2. This upgrade reflects improvements in MCB’s profitability and asset quality metrics as well as strong capital levels. The agency acknowledged its sound business model, alongside underscoring its disciplined expansion strategy, notably in Africa.

- In support of the above, entities of the Group capitalised on their robust risk management and internal control frameworks, which enabled them to identify, monitor and mitigate risk exposures in a consistent manner. Alongside improving the efficiency of processes and upgrading information systems, we tapped into enhanced synergies amongst relevant functions and entities. As a major undertaking, Group entities moved forward to ensure their readiness for the timely implementation of IFRS 9, notably the adoption of ‘Expected Credit Loss’ (ECL) models to determine allowances for credit impairment.

- Of key significance in view of its business development momentum and market diversification endeavours, MCB Group has invested in a digital platform to help further enhance its risk management framework, thus enabling the organisation to: (i) consolidate the Enterprise Risk Management methodology adopted across subsidiaries; (ii) formalise the documentation of the Group’s Risk Register comprising a description of each risk together with the measurement and recording of the inherent and residual risk exposures around key themes, namely Strategic, Financial, Operational and Compliance; and (iii) monitor the residual risk exposures and the mitigating controls in order to bring such exposures below tolerable levels.

-

MCB Ltd

- Mindful of the nature and materiality of risks to which it is being exposed, the Bank has pursued its growth endeavours in a healthy manner, alongside ensuring that strict adherence is fostered with updated and new regulatory stipulations. Towards meeting its objectives, MCB has, notably, strengthened its Permanent Control function to shore up its control mechanisms and assist business units in reinforcing their respective risk oversight. Key initiatives deployed include the following: (i) the Bank implemented a Permanent Control framework to ensure that critical controls are performed and are effective, thanks to a ‘Business Risk Correspondents’ level of control, with findings escalated to Management and Board; and (ii) a new approach for risk mapping has been launched for deployment across the Bank, with a view to identifying and assessing operational risks as well as ensuring that effective internal controls are implemented to address any major or critical issues identified. Worth noting also, the Bank further bolstered its Anti-Money Laundering/Fraud Prevention (AML/ FP) and Compliance functions to effectively manage related risks, with main measures as follows: (a) the Compliance function was reviewed, with the creation of five distinct clusters to ensure effective compliance coverage across business units/branches; (b) a gap assessment was conducted with a view to gearing up capabilities, notably in terms of relevant processes and systems, towards fostering the Bank’s compliance with the country’s Data Protection Act and advocated international standards, with a key case in point being the General Data Protection Regulation / Data Processing Agreement (GDPR/DPA); and (c) the efficiency of the customer onboarding process has been further improved. Furthermore, based on current state assessments, a list of gaps and compensating controls to be deployed across the Bank were identified to enhance its information security and increase resilience in case of cybersecurity breach. We reinforced our processes and frameworks to effectively mitigate cyber risks associated with the increased digitalisation of our operations.

-

Foreign banking entities

- Our foreign banking subsidiaries have further bolstered their ability to identify, mitigate and manage risks faced. As a key move, risk workshops and risk control self-assessments have been carried out by MCB Seychelles to identify business and operational risks classified under the following Basel themes: ‘Execution, Delivery and Process Management’, ‘Business Disruption and System Failures’, ‘Clients, Products and Business Practice’, ‘Employment Practices’ and ‘Workplace Safety, External and Internal Frauds’. Subsequently, MCB Seychelles developed an action plan to address deficiencies and bring down risk exposures to tolerable levels. Of note, MCB Maldives and MCB Madagascar are in the process of carrying out the same exercise during the current financial year. Moreover, our foreign banking entities have reinforced their system of Permanent Control and compliance certificates, with organisation structures, digital systems, procedures and dashboards designed to ensure that key controls are operating effectively and any exceptions are proactively approved, monitored and addressed. This initiative also involved refreshing all procedures and controls documentations across risk areas and assigning the ownership of key control environments to specific Managers and supervisors. Across entities, it can be noted that KYC remediation efforts have progressed satisfactorily, with a risk based approach being adopted to ensure that records of active customers are regularly updated. Concurrently, our automated risk-based due diligence platform, which is operational since August 2019, helped to consolidate further our AML risk monitoring framework. In addition, our cyber security environment was further strengthened during the period under review through the implementation of new infrastructure, tools and processes, complemented with comprehensive penetration and vulnerability testing carried out by external consultants. At the same time, our entities have pursued the testing of their business continuity management, disaster recovery and relocation processes, with a view to ensuring that our policies, procedures and processes are effective.

- At a specific level, MCB Seychelles embarked on a process of scanning and electronic archiving of contracts and other documents from relevant business units. This initiative was undertaken with a view to enhancing the protection of critical information pertaining to the bank and its customers as well as better managing its exposure to information risk, in line with data protection laws and regulations. Mindful of the challenging operating environment, MCB Maldives has reviewed the operating model underpinning its risk management architecture to embed improved efficiency levels. A key move relates to the reinforcement of staff operating in the information technology field so as to pave the way for the in-depth upgrade of the current infrastructure, cater for the independence of the function and foster alignment with Group standards. In the wake of the challenging operating environment to which it is exposed, MCB Madagascar shored up its frameworks and capabilities across the credit risk management cycle,as reflected notably by a strengthening of relevant processes for the assessment and monitoring of files being handled.

-

Other entities

- MCB Capital Markets Ltd (MCBCM) implemented specific measures to further strengthen its risk management and compliance framework. One notable example is the complete revamp of its induction process to inculcate a strong compliance culture right from the outset when employees join the company. This is reinforced by refresher modules that all employees are requested to complete online by set deadlines. Risk management processes have also been strengthened by reducing the instances of human intervention in certain critical processes. Within MCB Investment Management, enhancements to the core IT system have been made to facilitate attribution analysis, which is a critical tool in financial risk management. MCBCM has further reinforced its anti-money laundering framework following the adoption of the Financial Intelligence and Anti Money Laundering Regulations (2018), which repealed and replaced the Financial Intelligence and Anti Money Laundering Regulations (2003). In addition, the complaints handling procedures were reviewed, following the creation of the country’s Office of the Ombudsperson for Financial Services.

- While adopting judiciously-crafted enterprise risk management practices, MCB Consulting Services Ltd continued to capitalise on the diversification of its value proposition, with broad-based markets served across geographies, underpinned by the recruitment of staff with adequate and diverse skills sets. It anchored its growth strategy on well-structured foundations, including notably partnership agreements sealed with carefully-selected stakeholders. Worth noting also, the entity has set out to thoughtfully manage currency risks through the conduct of swap and forward transactions, while also tapping into its natural hedging strategy.

- International Card Processing Services Ltd (ICPS) has continued to reinforce its risk management framework, under the guidance of its Audit and Risk Committee. Since the past two years, ICPS has adopted an Enterprise Risk Management approach. In light thereof, business risks workshop have been regularly carried out to enable the organisation to manage the potential impact of risks permeating across all processes, activities, stakeholders as well as products and services. Leveraging on the framework and the appropriate culture, Enterprise Risk Management is a critical component of the entity’s plan-based strategy that aims to identify, assess and prepare for any risk that may interfere with its business development goals and objectives, in line with the changing business environment.

Looking ahead: Our key targets to anchor sound business growth

- Foster relevant reinforcements to the approach and frameworks for the identification, assessment, mitigation and management of risks across entities, alongside ensuring broad alignment of policies, control measures and practices across the Group

- Uphold the soundness of key financial metrics across entities of the Group, while adhering to legal and regulatory stipulations wherever applicable; ensure that business expansion endeavours, notably on the regional front, materialise in a sensible manner, backed by a close structuring of deals, adherence to an adapted risk appetite and systematic scrutiny of clients’ operating context

- Execute dedicated and proactive measures towards further strengthening our anti-money laundering platforms and policies; reinforce our compliance framework, while further bolstering client onboarding and monitoring processes (in alignment with local stipulations and advocated global norms and standards), backed by the increa sed automation and simplification of processes

- Continuously appraise and manage cyber risks, supported by relevant upgrades to our tools and processes

- Further embed the adherence to a sound risk culture across different layers of the organisation

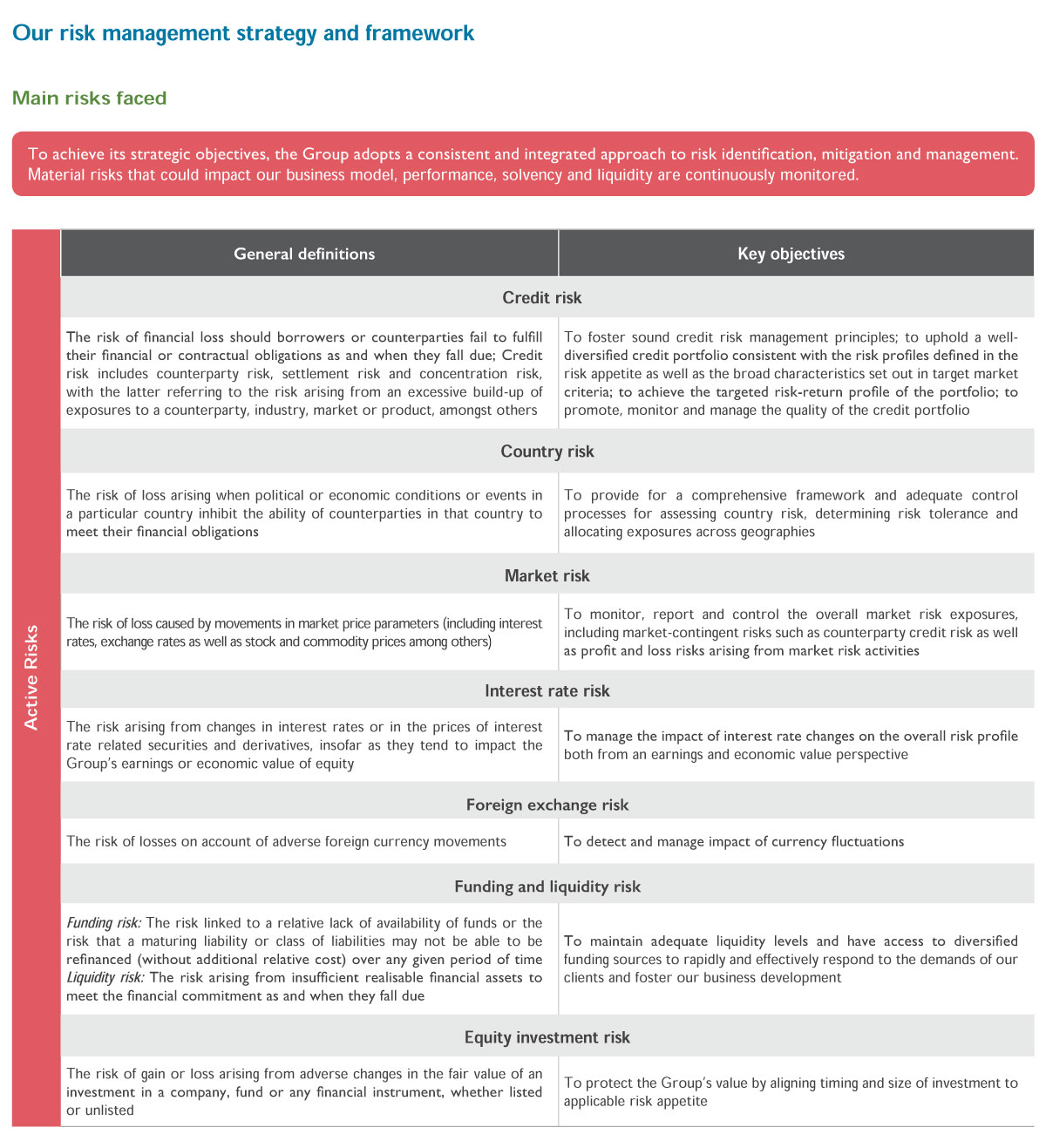

Financial soundness

Capitalisation

Philosophy

While ensuring that applicable and evolving regulatory requirements are met at all times, the capital management approach of the Group is to ensure that its subsidiaries are adequately capitalised to help achieve sound and sustained business growth, alongside protecting and maintaining the trust of shareholders and providers of fund.

Towards this end, the Group favours internal capital generation through retained earnings while being well positioned to tap into capital markets as and when required, on the basis of its status as the most liquid stock on the local stock exchange,. Moreover, it seeks to maintain appropriate discipline over the nature and extent of its market development initiatives and lays due emphasis on optimising the allocation of capital across businesses.

Performance

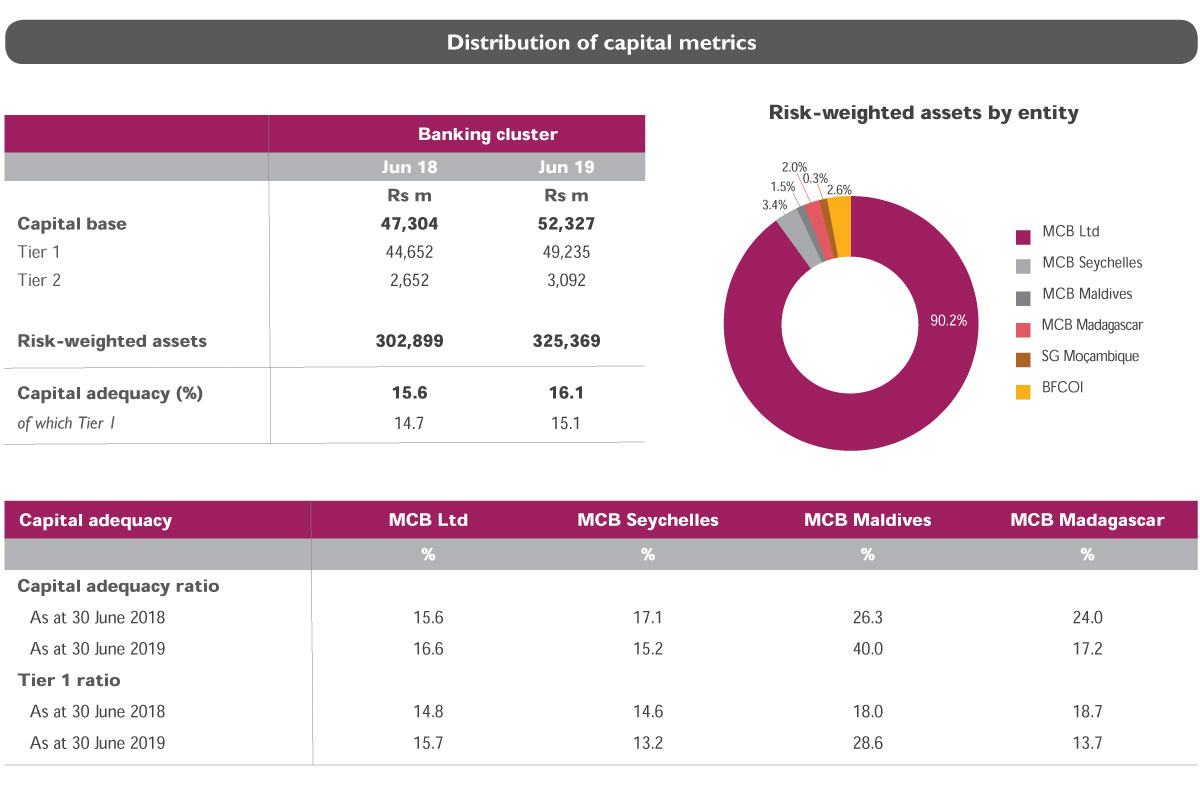

Over the period under review, the Group has, on a consolidated basis, maintained comfortable capitalisation levels as gauged by the BIS and Tier 1 ratios standing at 17.4% and 15.8% respectively as at 30 June 2019. The predominant contribution thereto has obviously emanated from the banking entities of the Group, for which the maintenance of adequate capital levels is a key priority by virtue of their business operations and regulatory responsibilities. The risk weighted assets of the Group stood at around Rs 348 billion as at 30 June 2019, out of which 85% was accounted for by MCB Ltd and some 6% by the foreign banking subsidiaries. The Group’s overseas associates, namely Société Générale Moçambique and Réunion-based BFCOI – whose investments have been risk-weighted at 250% in line with applicable Basel III rules – represented 3% of its overall risk-weighted assets.

Asset quality

Performance

Notwithstanding still challenging market conditions, the gross and net NPL ratios of the Group went down to 4.1% and 2.9% as at 30 June 2019. While notable improvements were observed at the level of MCB Seychelles and MCB Madagascar, the asset quality metrics of the Group were mainly supported by trends witnessed by MCB Ltd. Backed by its prudent market development approach and active recovery efforts, the gross NPL ratio of the Bank fell by around 30 basis points to reach 3.8% in FY 2018/19, with the corresponding ratio in net terms standing at 2.8%. The Group’s specific coverage ratio stood at 30.3% with the remaining portion being adequately covered by collateral, suitably discounted to reflect current market conditions and expected recovery time.

Whilst the Group’s impairment charges rose by some 20%, the cost of risk in relation to loans and advances dropped marginally to 59 basis points of the latter.

Credit Quality

Funding and liquidity

Philosophy

The Group seeks to keep sound funding and liquidity positions in support of its business development ambitions. While accessing wholesale markets as and when required, the banking entities of the Group maintain cost-efficient, diversified and stable sources of funding which predominantly comprise customer deposits. Furthermore, an appropriate level of liquid assets is kept to ensure that obligations can be met within a reasonable short-term time-frame.

Performance

The Group continued to be exposed to relatively high liquidity conditions in the Mauritian banking sector, with the situation also warranting attention in Madagascar, Maldives and Seychelles. Against this backdrop and while it preserved its sound funding position the Group continued to display relatively high liquid assets levels, as demonstrated in the following illustrations. In this regard, the consolidated Liquidity Coverage Ratio of MCB Ltd stood at 400% as at 30 June 2019, which comfortably overshot the applicable regulatory limit. Besides, though not yet a regulatory requirement in Mauritius, MCB reported a Net Stable Funding Ratio of 123%, which exceeds the minimum level recommended under Basel III, set to be at least 100% on an ongoing basis. As a key funding initiative, MCB Ltd has, in April 2019, signed a USD 800 million Dual Tranche Syndicated Term Loan Facility through general syndication. It comprises two tranches, with Tranche A having a tenor of 1 year and Tranche B having an initial tenor of 2 years, with a 1 year extension option at the Borrower’s discretion. The objective is to help the Bank execute on its African ambitions, while further optimising and diversifying its funding profile.

Our business model

Key principles

Stakeholder engagement

Our risk policies make allowance for the long-term interests of our customers, regulators and other stakeholders

While achieving sustained business growth, we help our stakeholders realise their ambitions and prosper

Key elements of our risk management set-up

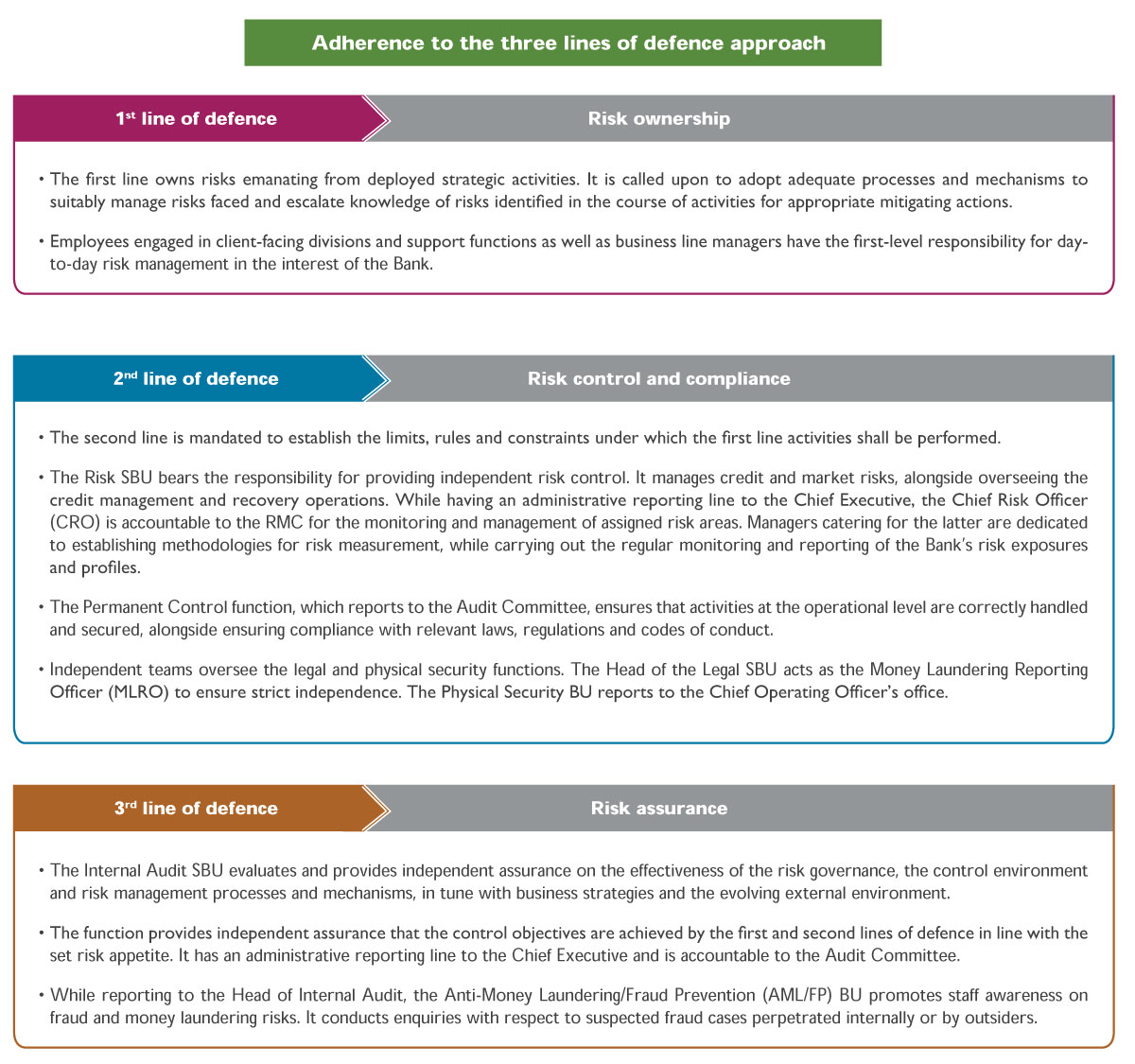

Governance and oversight

• Underpinned by the establishment and enforcement of clear lines of responsibility and accountability throughout the organisation, it ensures that relevant procedures and practices are in place in order to protect the Company’s assets and reputation. For the discharge of its duties, the Board is assisted by committees which enable it to properly formulate, review and approve policies on monitoring and managing risk exposures.

• The RMC monitors risk portfolios against set limits with respect to, inter alia, risk concentration, asset quality, large and foreign country exposures, in compliance with regulations and internal policies.

• The Audit Committee caters for the monitoring of internal control processes, while ensuring the preparation of accurate financial reporting and statements in compliance with applicable legal requirements and accounting standards. It also reviews operational and compliance risks and the actions taken to mitigate them.

• The Supervisory and Monitoring Committee continuously oversees the overall management of the Group and is also responsible for the ongoing monitoring of the Group’s performance against set objectives.

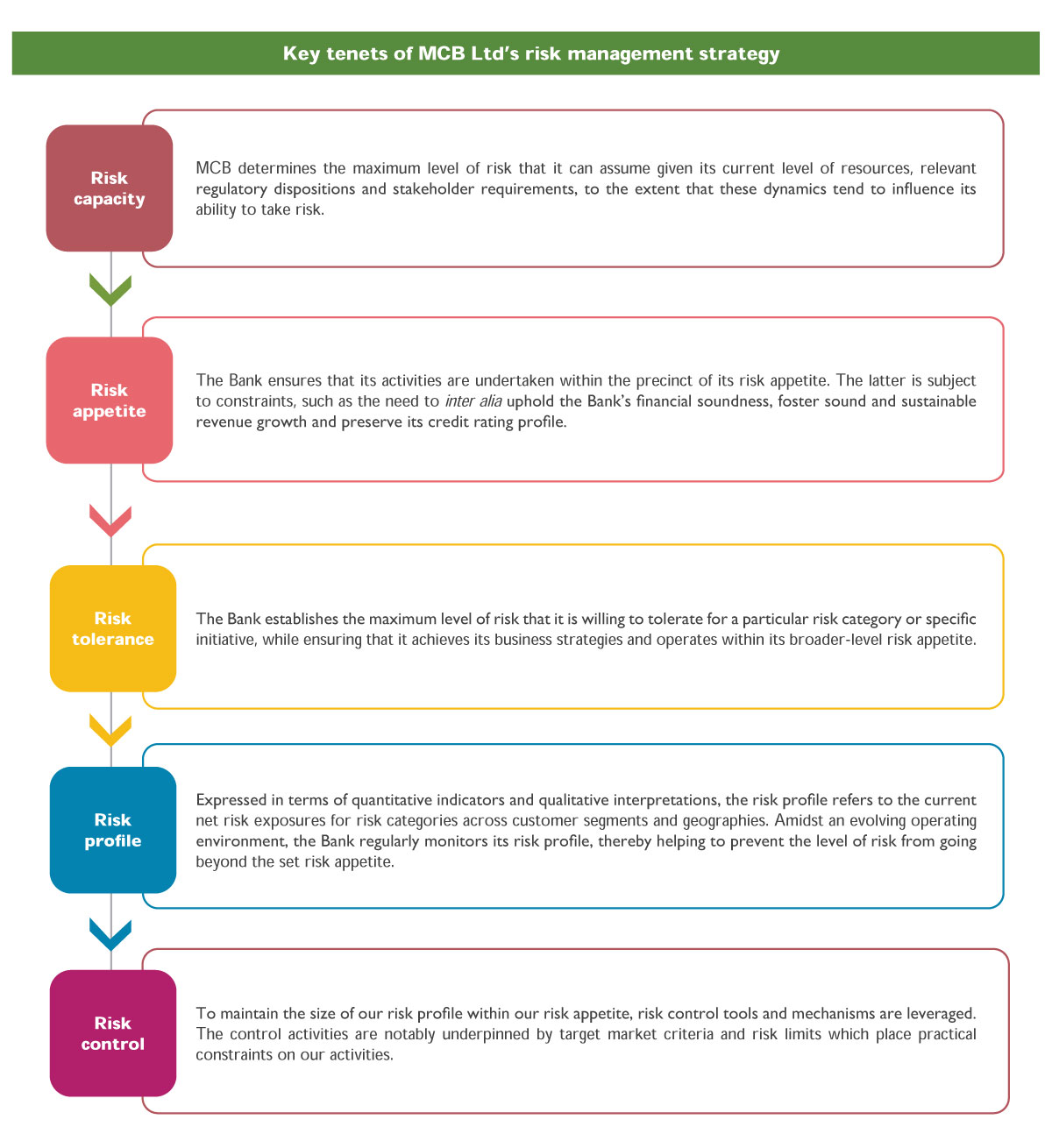

Our risk appetite framework

-

Framework

- The Bank articulates and monitors its risk appetite on the back of its solid framework and processes. They provide an informed guidance for the management and monitoring of our risk profile in relation to the defined riskappetite, alongside promoting the sound execution of our growth agenda.

- The purpose of setting risk appetite is not necessarily to limit risk-taking, but to align the Bank’s risk profile and strategic orientations. Its risk appetite is regularly updated to reflect stakeholder aspirations and the context.

-

Key underpinnings

- MCB inter alia defines its risk appetite for (i) credit risk in terms of allocation of range targets for domestic and international credit exposures, exposures by sectors as well as risk profiles and asset quality of portfolios; and (ii) market risk in terms of the splits between domestic and international markets, foreign currency and interest rate exposures, exposure allocation for position-taking and target splits in terms of exposure maturities.

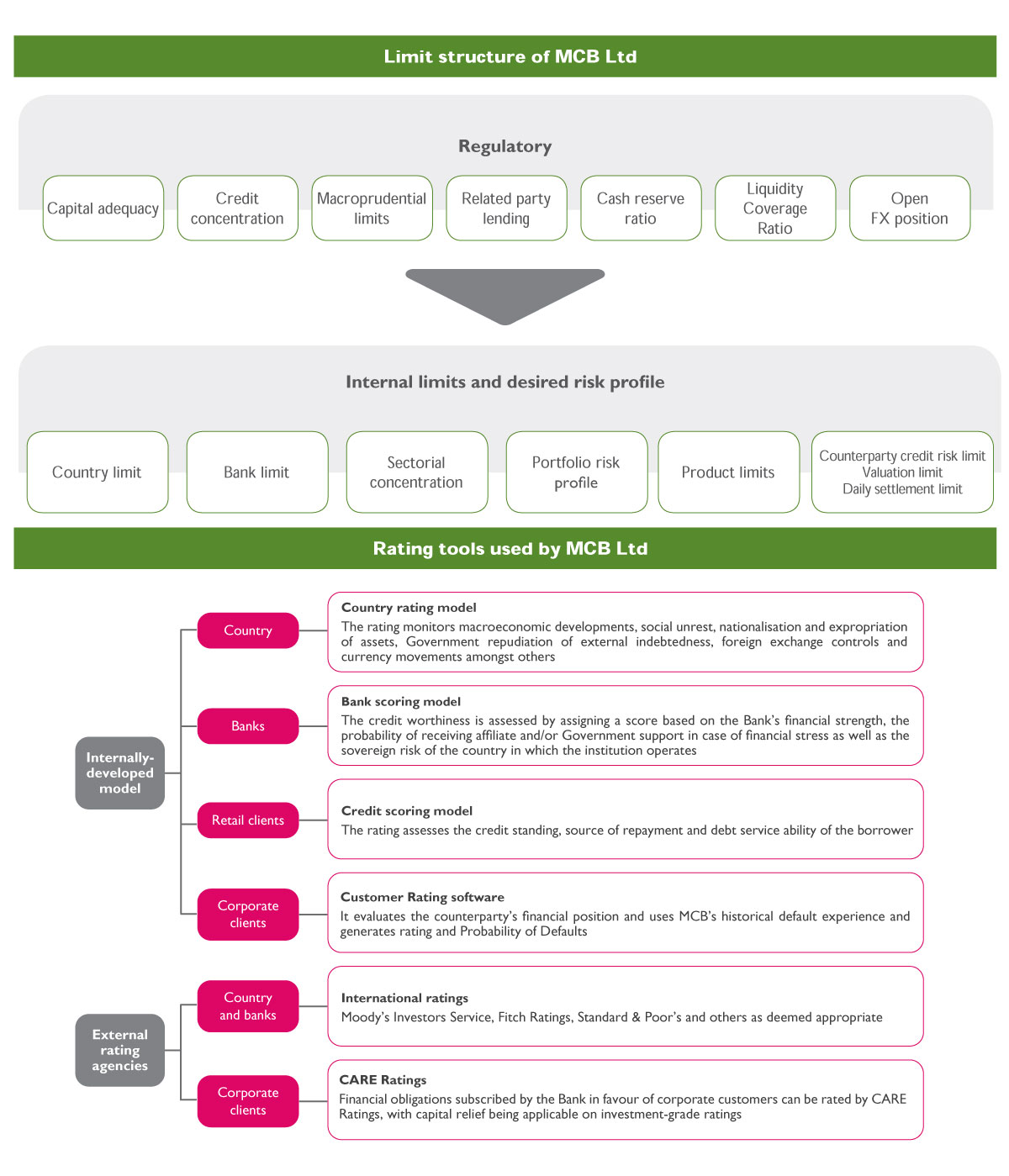

- For proper risk identification and quantification, the Bank caters for: (i) continuous monitoring of risk targets; (ii) quarterly risk reporting to RMC; (iii) preparation of risk reports for capital management; and (iv) the application of a stress-testing framework. The size of the internal risk limits is a function of regulatory requirements and the risk appetite set by the Bank, after making allowance for the relevant economic and market environments. In its day-to-day business, the Bank makes use of internally-generated and externally-sourced rating tools for the purpose of risk identification, quantification and monitoring.

Governance

Board of MCB Ltd

- The Board of MCB Ltd has the ultimate responsibility for ensuring adequate risk management across the Bank, in line with good corporate governance principles. It provides clear guidance for the setting out and regular review of applicable strategic thrusts, processes and policies for risk management.

- As a key focus area, the Board is responsible to validate the Bank’s risk appetite towards achieving its objectives. It delegates authority to Board committees, which formulate the specific responsibilities and required policies for effective risk management.

Board Committees

Executive committees

Active risks

Credit risk

|

Executive Credit Committees (ECC)

|

|

|

Credit Committee (CC)

|

|

|

Country Risk Committee (CoRC)

|

|

Market risk

|

Asset and Liability Committee (ALCO)

|

|

Passive risks

|

Information Risk, Operational Risk and Compliance Committee (IORCC)

|

|

Foreign banking subsidiaries

Board and its committees

- The respective Boards exercise their responsibilities in respect of risk management through (i) the oversight of the risk governance process, including setting risk appetite in line with Group-level orientations; (ii) regular and comprehensive assessment of risks; (iii) the maintenance of sufficient capital adequacy levels in alignment with the Group’s framework, the internally-set risk appetite and regulatory requirements; and (iv) clear delegation of authority to relevant committees and management.

- Risk management matters are reported to the Board of each foreign entity through their respective committees, namely the Audit Committee and the Risk Monitoring Committee, while major issues identified are also escalated to the corresponding Board committees of MCB Group

Ltd. The management teams of the entities are responsible for conducting business within the strategic framework and risk appetite set by their Board, while monitoring risk portfolios through dedicated committees.

Executive committees

Key responsibilities

|

Subsidiary Credit Committee

|

|

|

Asset and Liability Committee

|

|

Credit risk

With regard to the determination and review of impairment and provisioning levels, the banking entities undertake their respective exercises on a regular basis, while being subject to appropriate oversight. The entities adhere to relevant regulatory stipulations, alongside aligning themselves to advocated standards. At the level of MCB Ltd, the exercise is undertaken on a quarterly basis and involves the collaboration of several stakeholders. After being reviewed and agreed upon by the RMC as well as validated by the Board, the figures are submitted to the Bank of Mauritius (BoM). The BoM Guideline on Credit Impairment Measurement and Income Recognition aims at aligning regulatory prudential rules as regard asset classification and provisioning requirements with international accounting norms (i.e. IFRS 9). The aim is to ensure that financial institutions have adequate processes for determining allowance for credit losses in a timely manner and the carrying amounts of credit portfolio recoverable values. While ensuring adherence to prudential norms which define credit as impaired if it is past due for more than 90 days, the Bank also assesses facilities granted to clients as being impaired on case-by-case basis above a certain materiality threshold. Furthermore, loans are written off by the Bank when the prospect of recovery is poor and the loss can be reasonably determined, with MCB complying with the BoM guideline for the write-off of non-performing assets.

MCB ltd: Adoption of IFRS 9

- In July 2014, the International Accounting Standards Board (IASB) issued the ‘International Financial Reporting Standards 9, Financial Instruments’ (hereinafter referred to as IFRS 9), in order to replace the ‘IAS 39, Financial Instruments – Recognition and Measurement’. The new standard became effective for the year beginning on or after 1 January 2018.

- In 2017, to facilitate the implementation of the new standard, MCB set up an executive Steering Committee to oversee the adoption of IFRS 9 and the application of related requirements within the accounting and risk management functions of the Bank. A Technical Review Committee – comprising independent experts from the Bank’s external auditors, project sponsors and an appointed accounting firm – was set up to ensure full compliance with applicable requirements. Progress was monitored at various levels and regular reporting was undertaken to the Risk Monitoring Committee (RMC) and the Board, with the Bank of Mauritius being also apprised of ongoing developments. Once the project was completed, the Bank set up a dedicated Credit Modelling BU, operating under the aegis of the Chief Risk Officer – in order to develop, maintain and validate models for credit application, Basel Capital Accord reporting and IFRS 9 modelling purposes.

IFRS 9 implementation'

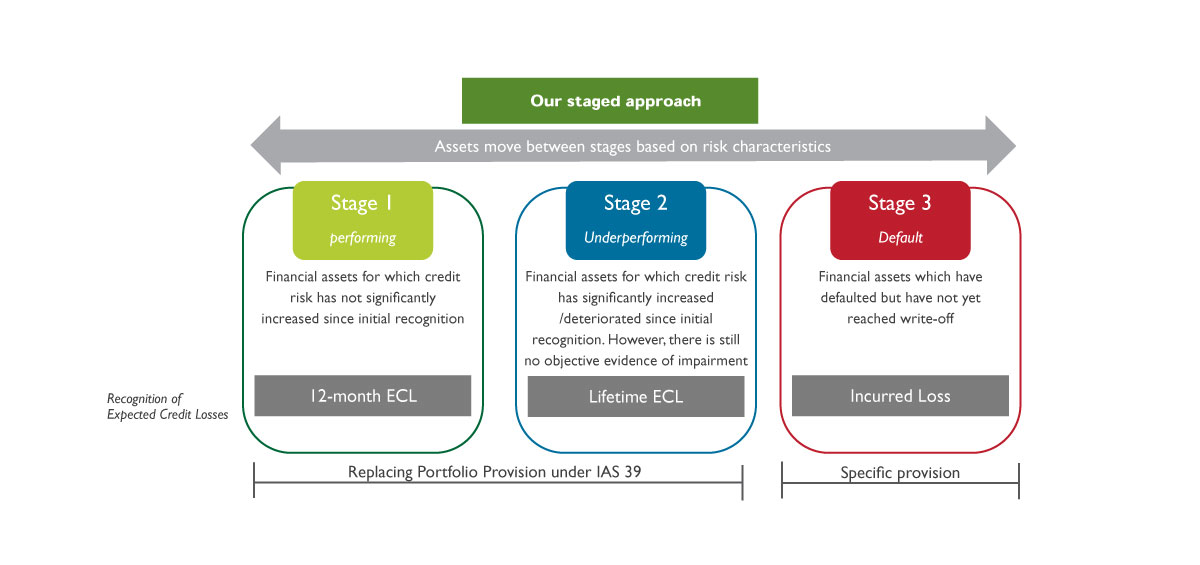

- IFRS 9 replaces the incurred loss model (whereby losses were recognised when a default event occurred) with an Expected Credit Loss (ECL) Model. This implies that provisions are calculated upon recognition of financial assets, based on the potential losses expected on the latter. Of note, the standard also requires off-balance sheet items be taken into account in determining ECLs.

- In measuring ECL, three main parameters are considered and estimated, namely: (i) Probability of Default (PD), which represents the likelihood of a default event occurring; (ii) Loss Given Default (LGD), which denotes the estimated losses in the event that a default event occurs; and (iii) Exposure at Default (EAD), which reflects the exposure at risk at a point of default. In addition, IFRS 9 requires that allowance be made of forward-looking information in the calculation of ECL, taking into consideration past, actual and future insights on customer behaviours and macroeconomic indicators.

- IFRS 9 introduces a three-stage approach to the impairment calculation of financial assets. To determine the staging status of the asset, IFRS 9 requires an assessment of whether or not there has been a significant increase in credit risk since initial recognition. This dictates the basis on which its ECL is calculated, as illustrated below.

1 Information in this section has been audited

- In determining whether there has been significant increase in credit risk or credit deterioration, an entity considers reasonable and supportable information that is relevant and available without undue cost or effort. At MCB, quantitative and qualitative information are taken into account, based on the Bank’s historical customer experience and credit risk assessment. A financial asset is credit impaired and is in Stage 3 when (i) contractual payments or accounts in excess are past due by more than 90 days; and/or (ii) other quantitative and qualitative factors indicate that the obligor is unlikely to honour its credit obligations.

- MCB segmented its financial assets into nine portfolios for ECL calculation, which are described as follows: (i) Retail: housing loans, other secured loans, unsecured and revolving facilities, SMEs; and (ii) Wholesale: corporate, financial institution, sovereign, project finance, and Energy & Commodities.

Retail: PD, LGD and EAD parameters are calculated on a portfolio-based approach, i.e. facilities having homogeneous characteristicss are assumed to have similar risk behaviors and can reasonably be assigned same parameter values.

Wholesale: MCB uses a combination of internal models and external benchmarking for the calculation of PDs, LGDs and EADs. Internal historical default rates and losses have been used to calibrate PDs and LGDs respectively. For portfolios where MCB has historically experienced low or no default, external benchmarking has been used for calibrating corresponding ECL parameters. Of note, PDs leverage ratings model for all wholesale portfolios, which is mapped to an Internal Master Rating Scale. As for EAD calculation, either amortisation schedules or historical data and regulatory credit conversion factors have been used as EAD ratios.

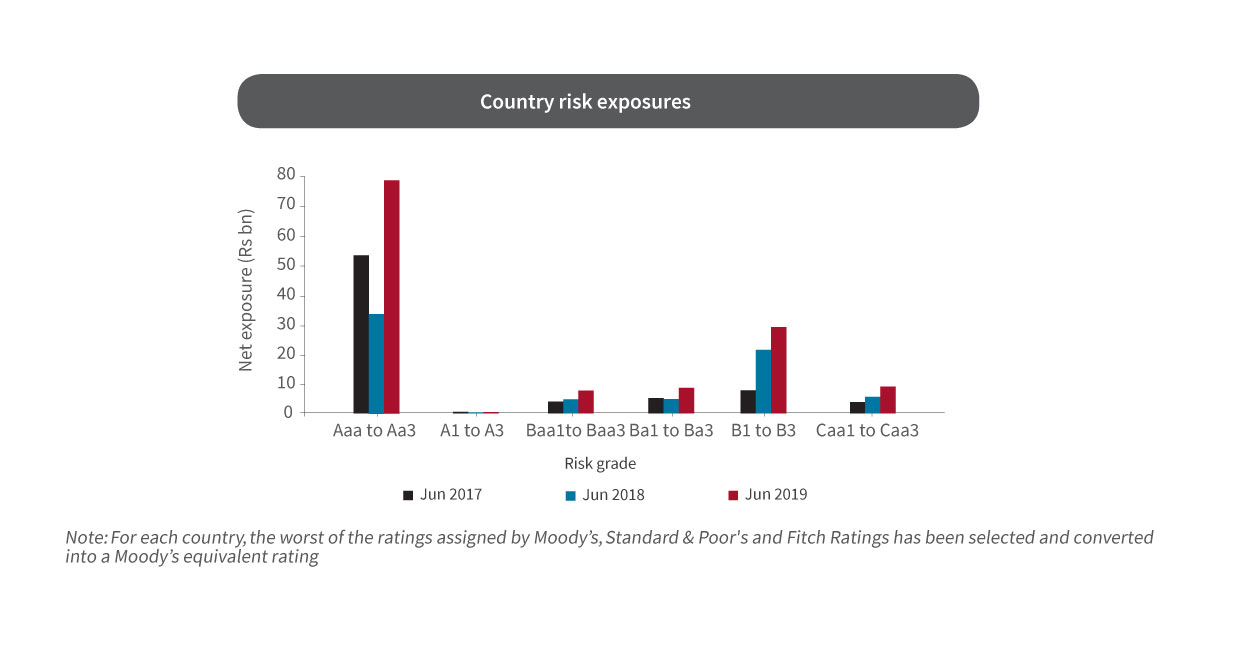

Country risk management at MCB Ltd

As regard the foreign exposures of MCB Ltd, the latter adopts a well-calibrated framework and related policies and processes to effectively manage its country risk. In fact, in the wake of continuous headway made in expanding its footprint in the region, the Bank ensures that its activities are undertaken in a disciplined and balanced way. As a key priority, the Bank applies a robust risk management approach to assess country risk, deploy its activities and monitor exposures across markets

Market risk

Market risk

Cash flow management

- The entities maintain a continuously maturing stream of assets and liabilities through time, while avoiding undue accumulation of maturities in any one time band, especially those expected to mature in the near future.

- They use cash and liquidity gap profiles in both local and significant foreign currencies to monitor the impact of projected disbursements by lines of business. They undertake the behavioural analysis of their non-maturity deposit base in order to assign an actuarial maturity profile thereto, while ensuring that historical stickiness remain within non-volatile ranges.

Liquid assets buffer maintenance

- The entities hold a stock of high quality and unencumbered assets consisting of cash or quasi-cash instruments, with high convertibility characteristics. The aim is to meet unexpected outflows of funds or substitute expected inflows of funds (such as loan instalments) that do not eventually materialise by disposing of such assets at little or no loss in market value.

Funding management

- The entities maintain diversified liability bases across different categories of depositors, alongside also covering a spectrum of short to medium term funding.

- MCB Ltd resorts to wholesale markets whenever required. It capitalises on the technical experiences as well as the relationships developed by dedicated teams dealing with financial institutions and banks. Of note, in April 2019, MCB signed a USD 800 million Dual Tranche Syndicated Term Loan Facility through general syndication. It comprises two tranches, with Tranche A having a tenor of 1 year and Tranche B having an initial tenor of 2 years, with a 1 year extension option at the Borrower’s discretion. The proceeds from the syndication are being used for general corporate purposes. The objective of this exercise is to help the Bank execute on its African ambitions, while further optimising and diversifying its funding profile.

MCB Ltd : Key Liquidity Ratios

Liquidity Coverage Ratio (LCR)

- Introduced as a key standard under Basel III, the objective of the LCR is to promote the short-term liquidity resilience of a bank by ensuring the latter maintains an adequate stock of unencumbered High Quality Liquid Assets (HQLA) to meet its short-term liquidity requirements under a crisis scenario. The Bank of Mauritius Guideline on Liquidity Risk Management is closely aligned to Basel norms. It defines the LCR as the ratio of the stock of HQLA to the total net cash outflows over the next 30 calendar days. The transitional arrangements set out by the Central Bank for the evolution of stipulated ratios are described in the following table.

- As at 30 June 2019, the Bank comfortably overshot stipulated LCR requirements. It reported a consolidated LCR of 400%, which is equivalent to a surplus of around Rs 80 billion over stressed total net cash outflows. At a more granular level, we exceeded the mandatory LCR limits relating to rupee and significant foreign currencies. It can be noted that HQLA eligible for the purpose of calculating the LCR under the BoM guideline consist of cash or assets that can be converted into cash at little or no loss of value in private markets. On this note, it can be observed that MCB has, during the last financial year, maintained suitable levels of unrestricted balances with the Bank of Mauritius as well as investments in Central Banks and sovereign securities.

Net Stable Funding Ratio (NSFR)

- Under Basel III, the NSFR aims to promote the resilience of a bank over a longer time horizon by requiring the latter to fund its activities with sufficiently stable sources of funding in such a way as to mitigate any future funding stress. The NSFR effectively recognises a bank’s maturity transformation role in the credit creation and resource allocation process. It seeks to limit its overreliance on short-term wholesale funding or the running of large funding gaps to sustain rapid balance sheet growth.

- Though not yet a regulatory standard in Mauritius, MCB regularly monitors its performance in terms of NSFR, which requires an amount of available stable funding to be maintained in relation to required stable funding. As at 30 June 2019, MCB Ltd reported an NSFR of 123%, which exceeds the minimum level recommended by Basel III, itself set to at least 100% on an ongoing basis.

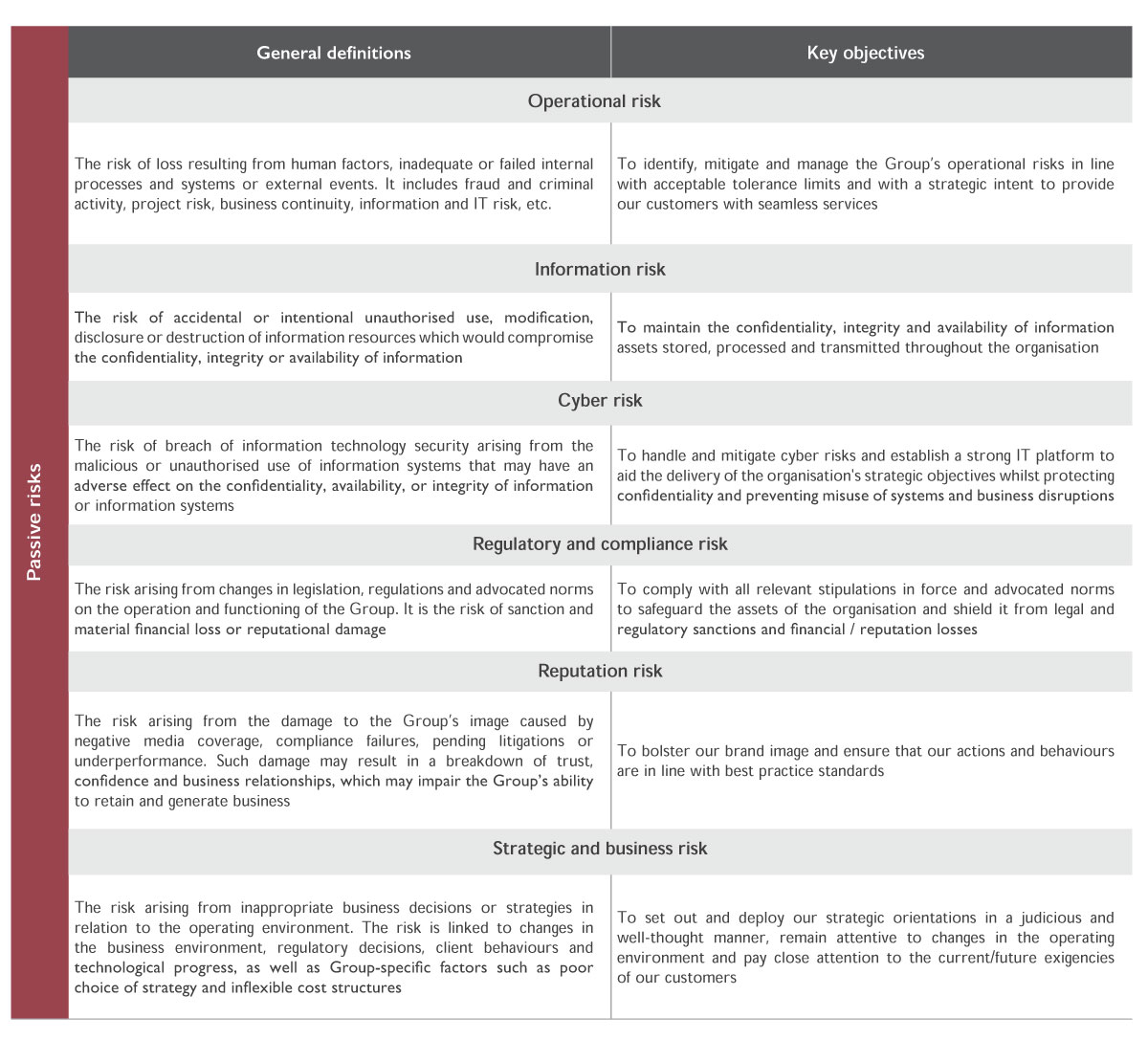

Operational risk

General approach

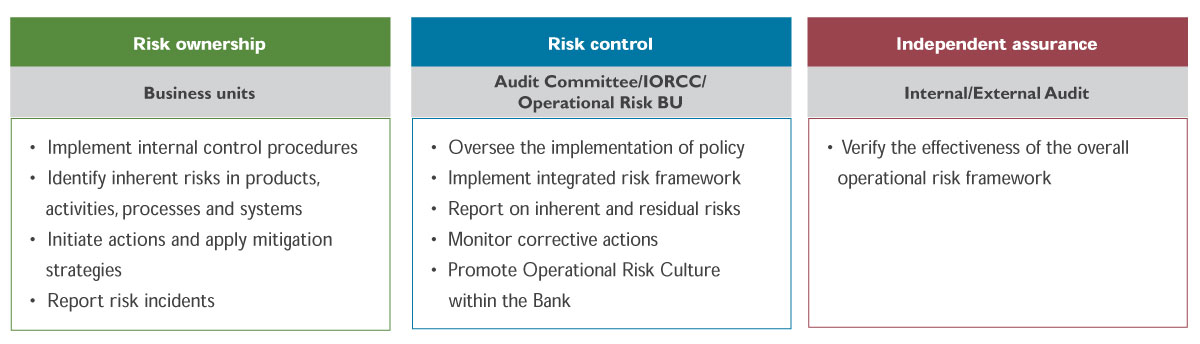

- The banking entities of the Group aim to identify, mitigate and manage operational risks across their activities, processes and systems in line with the defined risk tolerance. The objective is to underpin the continuity of their operations and anchor a solid platform to provide customers with seamless services.

- Towards determining the operational risk tolerance levels, the entities set risk acceptance and mitigation limits in respect of the principal categories of operational risk as appropriate. Operational risk sanctioning mandates and day-to-day oversight responsibilities are entrusted to Management. The latter is responsible for the application and effectiveness of the operational risk policy. The key duties are to (i) ensure compliance with underlying objectives set in terms of the management of such types of risk; and (ii) foster the development, implementation and documentation of internal controls and processes.

- The operational risk management framework is anchored on adapted policies which are approved by the Audit Committee of each banking entity. At the level of MCB Ltd, the Operational Risk Policy of the Bank formulates the principles and methodologies for the management of operational risk at the Bank. It sets out a framework covering advocated rules and norms on the local and international fronts, best practices and standards as well as the relevant roles and responsibilities within the Bank. The latter’s operational risk management approach is governed by regulatory requirements, including the Guideline on Operational Risk Management and Capital Adequacy Determination.

Risk measurement and monitoring

- The determination of the risk exposures of the banking entities is anchored on the regular review of the operational risk inherent in their processes and client solutions, with the monitoring thereof performed against acceptable tolerance limits.

- With respect to MCB Ltd, as from FY 2018/19 and following the approval of the Bank of Mauritius, it applies the Alternative Standardised Approach for calculating and reporting its operational risk capital charge instead of the Basic Indicator Approach as was previously the case.

Risk mitigation and management

- At the level of MCB Ltd and as described in its Operational Risk Policy, the responsibility for implementing the Operational Risk Management Framework is entrusted to Senior Management. The Operational Risk BU is responsible for the implementation of policies for the identification, assessment and management of related risks. From a more holistic angle, operational risk management forms part of the dayto- day responsibilities of the Leadership team and employees at all levels of the organisation. Operational risk mitigation relies on appropriate policies, processes and systems, backed by the clear segregation of duties, dual control as well as the regular verification and reconciliation of transactions. The control environment is also based on an appropriate risk culture which is fostered through risk awareness sessions targetingrelevant audiences. An overview of both operational risk and Business Continuity Management is provided to new staff at the onset of their

career through induction courses. The Operational Risk Management Framework relies on three primary lines of control as depicted below.

As regards the foreign banking entities, they have reinforced their system of Permanent Control, alongside adhering to clearly-defined procedures and dashboards for controlling and mitigating the effects of operational risks faced. Moreover, the introduction of compliance certificates to be submitted monthly by the business units provides assurance that the identified controls are functioning adequately. The management of operational risks by the entities is also underpinned by recourse to specific tools and systems that are adopted by MCB Ltd, notably the incident reporting system, as tailored to the subsidiaries’ business realities. In addition, staff leverage training courses, whereby the IT SBU as well as the Anti-Money Laundering/Fraud Prevention BU from MCB Ltd provide assistance on specific risk management needs.

MCB Ltd: Business Continuity Management (BCM) Framework and

Framework and accountabilities

- Business Continuity Management at MCB is defined as its ability to effectively plan for and respond to incidents and business interruptions to maintain the availability of the Bank’s critical activities at acceptable pre-defined service levels, thus safeguarding its reputation and the interests of key stakeholders. The framework is detailed in the BCM policy and outlines the prevailing governance structure as well as the roles and responsibilities of each actor involved in the BCM programme. As an integral part of the Operational Risk Management Framework in place at the Bank, the BCM framework is centrally coordinated and controlled by the Operational Risk BU, in collaboration with relevant support functions.

- A dedicated crisis management team consisting of key members of Senior Management shoulders central command during a crisis, while being assisted by several tactical and operational crisis teams. Individual business units, through designated business continuity champions, are the BCM process owners and are responsible for designing, reviewing and maintaining up-to-date recovery plans at their respective levels.

Key progress during the last financial year and until recently

- During the period under review, MCB has further consolidated its business continuity preparedness and resilience to reflect changes in the business landscape and ensure that mission critical activities are able to resume in accordance to defined objectives and stakeholder expectations.

- MCB integrated the Disaster Recovery, Emergency Response and Crisis Management Disciplines within its BCM framework. Lately, the Bank proceeded with its annual Disaster Recovery simulation exercise to test the operability of its critical systems hosted on servers located at its Disaster Recovery site. As a key move, the Bank integrated pandemic planning in its BCM framework to better shape its response during a disease outbreak, thus ensuring that impact on people and operations are mitigated. A Disease Outbreak and Pandemic Preparedness Policy, which is aligned with international standards, was approved by the Board, with related procedures and guidelines being disseminated to all staff as required.

- The Bank embarked on the automation of its BCM processes through the acquisition and roll-out of a dedicated software to be gradually extended across Group entities. The objective of this exercise is to further improve conditions for updated business continuity plans and procedures to be readily accessible during a crisis to ensure that the Bank can resume its critical operations smoothly and within identified Recovery Time Objectives.

Information risk

General approach

The entities adopt a dedicated approach to uphold their information security, alongside ensuring that they are prepared to respond to potential cyber-attacks and threats to its information assets in a timely and effective manner. They conduct regular assessments to identify issues that can potentially harm its assets, with adequate mitigating controls being deployed.

Risk mitigation and management

- Risk management by the banking entities implies the regular conduct of information risk assessments so as to identify issues that can potentially harm the organisation’s information assets and recommend adequate mitigating controls.

- At MCB Ltd, the Information Risk Management (IRM) BU is responsible for developing and maintaining information security policies, in line with the evolving operating landscape as well as requirements set by the authorities and other stakeholders. The key objective is to ensure that an adequate level of security is maintained to protect private and confidential information held by the Bank. To mitigate and manage risks faced, several processes have been assigned to assist in identifying and analysing the business need to access logical information, restrict the information deployed to the relevant requirements as well as monitor and control access to such information. The pertinence of any major information security expenditure is evaluated and discussed at several hierarchical levels before finally escalating to Senior Management and, if needed, to the Board for approval.

- The banking entities remain intent on gearing up their policies and processes to effectively cope with challenges posed by increasing cyber threats. For instance, at the level of MCB Ltd, several initiatives have been deployed to strengthen and ensure the robustness of its information security: (i) the Bank enhanced its security events monitoring and response capabilities, which have been regularly tested; (ii) MCB’s critical infrastructure (which includes customer-facing applications) has been independently tested and assessed from a security perspective; (iii) actions have been taken to enhance the staff’s cyber security awareness in order to recognise and properly react to cyber-attacks; (iv) the Bank’s compliance to laws and regulations relating to data protection has been regularly assessed with a view to identifying any gaps and gearing up its capabilities to adhere to relevant stipulations; (v) the set of critical controls underpinning MCB’s cyber security resilience were continuously monitored; and (vi) the risk assessment framework and information security management systems and processes were upgraded to foster alignment with internationally-recognised standards. As for our foreign banking entities, dedicated initiatives were taken to enhance the protection of critical information pertaining to the bank and its customers, in line with relevant laws and regulations.

Compliance risk

General approach and objectives

- The Group seeks to ensure that the organisation and its staff adhere, at all times, to both the letter and spirit of applicable laws, rules and regulations, generally accepted business and industry standards, as well as advocated norms and codes.

- The Group promotes a compliance-oriented culture with a view to supporting entities and business lines in delivering fair outcomes for customers and preserving the organisation’s reputation, while helping to achieve business development objectives.

Risk mitigation and management

- The banking entities seek to ensure that their core values and standards of professional conduct are maintained at every level and within all their activities and operations. Towards this end and in addition to complying with relevant external norms and requirements, they adhere to their own policies, including those related to their ethical standards. They adopt dedicated systems and processes so as to properly identify and prevent any risks of non-compliance while ensuring that they are sufficiently equipped to effectively cope with greater scrutiny by regulators and law enforcement authorities. In order to ensure that their objectives are met in a consistent and judicious manner, they perform regular monitoring exercises, to foster compliance with policies and procedures and ascertain that controls are operating in a sound way.

Core principles guiding compliance risk management

- Paying continuous attention to and undertaking regular reviews of ongoing developments as regard laws and regulations; accurately understanding their impact and coming up with necessary responses to effectively address the risks arising from such changes

- Fostering a coherent compliance control mechanism to pave the way for normalised processes and operations Maintaining a set of policies to promote strong ethical behavio ur by staff as well as to prevent and manage conflicts of interests

- Promoting awareness of Management and staff on requirements arising out of new/amendments to laws and regulations and other compliance-related matters (e.g. training sessions conducted last year with regard to matters pertaining to Anti-Money Laundering/ Combating the Financing of Terrorism, targeting some 1,000 employees across MCB Ltd)

- Providing adequate training to the compliance officers to ensure that they have the necessary knowledge and skills to fulfil the ir duties

- Maintaining close working arrangements and communication with business lines through the dissemination of compliance-related information,provision of advisory services and delivery of dedicated training courses to staff

- Fostering trusted relationships with regulatory and supervisory bodies by maintaining productive and value-adding dialogue with them to uphold effective two-way communication

In relation to their Anti-Money Laundering /Combating the Financing of Terrorism (AML/CFT) obligations, the banking entities of the Groupensure that adequate processes, systems and controls are in place to render their services inaccessible to criminals, including money launderers and terrorists or their financiers, alongside paving the way for detecting suspicious activities. While fostering continuous staff awareness, the entities inter alia ensure that employees are given appropriate training on AML/CFT and fraud prevention topics to help them identify suspicious transactions. A Financial Crime Risk Management system has been implemented for underpinning the oversight of anti-money laundering. Moreover, the entities adhere to a Whistleblowing Policy, whereby an alternative reporting process is established for use by all employees in confidence, without the risk of subsequent retaliation, victimisation, discrimination or disadvantage. The Whistleblowing Framework at the organisation is designed to assist employees deemed to have discovered malpractices or impropriety.

The compliance frameworks of our banking entities have been reinforced through the adoption of continuous permanent control mechanisms. Our overseas banking entities are assisted by the Compliance BU of MCB Ltd via the following forms:

Key areas of support by MCB Ltd to overseas entities

- Compliance risk assessments: It extends support to the Compliance Officers of the entities in the performance of compliance risk assessments and through compliance-related training provided to them

- Advisory services: It maintains an open line of communication with afore-mentioned Compliance Officers and encourages them to seek advice/guidance whenever they are in need of same

- Staff training: It provides AML/CFT training to staff of the entities when called for, in addition to reviewing materials that the Compliance Officers have prepared for the purpose of staff training

- Compliance monitoring: It elaborates compliance monitoring programmes whereby the Compliance Officers have to perform compliance tests, prepared at the level of the Compliance BU, to ascertain adherence to procedures

- Project execution: It assists entities embarking on the implementation of IT tools to ensure compliance risk management

- Other areas: It reviews operational procedures to ensure that they meet set standards and that all applicable legal and regulatory requirements are incorporated therein. Its services are also solicited where regulatory issues have to be resolved

Risk Assurance: Internal Audit

General approach

- The aim of internal audit at the Group level is to assess the policies, methods and procedures in place at the organisation in order to cater for their adequate application. Independent assurance is provided on the quality and effectiveness of internal control, governance and risk management systems and processes, thus helping to protect the organisation and its reputation.

- The established framework of the internal audit activity is risk-based. As a key thrust, the banking entities of the Group aim to gather the necessary audit and risk insights in order to support their strategic orientations.

Strategy and objectives

In line with good governance principles, the Internal Audit SBU of MCB Ltd reports to the Audit Committee, which approves and monitors the internal audit plan and recommendations. The key pillars which the function relies upon to roll out a disciplined approach to evaluate and improve the effectiveness of risk management and control processes are: (i) the implementation of regularly updated audit work programmes addressing, as far as possible, identified residual audit risks; (ii) increased usage of data analytics through a world-wide recognised audit software; and (iii) automation of tasks namely relating to time sheets, reports preparation, working papers and follow-up of recommendations. Based on its assessments, the Internal Audit function is presently not aware of any significant area of the Bank where there are no internal controls. The function does not believe that there are deficiencies in internal controls that could give rise to risks that could eventually jeopardize the operations of the Bank.

Capital management

The framework

Our process

Internal Capital Adequacy Assessment Process of MCB Ltd

Framework

Assessment and planning

Our capital position

Performance of the consolidated banking cluster

During FY 2018/19, the banking entities have maintained their respective capital adequacy ratios comfortably above the applicable regulatory requirements. The capital adequacy ratio of the banking cluster – as measured at the level of MCB Investment Holding Ltd on a consolidated basis – increased by around 50 basis points to reach 16.1% as at June 2019. The capital base was primarily made up of core capital, with the Tier1 ratio standing at 15.1% as at June 2019, up from 14.7% a year earlier. The following illustrations depict the capital adequacy ratios posted by the banking cluster and shed light on the distribution of risk-weighted assets by entity.

Non-banking clusters

Key principles and considerations for risk management

Legal and regulatory

-

Regular review of applicable laws and regulations to identify compliance gaps;

-

Active involvement of MCBCM’s Risk & Compliance (R&C) and legal teams in the development of new products and services to ensure that they are in compliance with applicable laws and regulations prior to being launched;

-

Monitoring of changes to the legal and regulatory framework and initiation of corrective actions as necessary; and

-

Bi-annual monitoring exercises undertaken by the R&C team to assess the level of compliance with laws and regulations, particularly with respect to anti-money laundering.

Operations (people, processes and systems)

-

A significant proportion of R&C’s resources is allocated to the management of operational risks. The methodology, which places particular emphasis on high volume businesses, is set out below.

-

The initial stage of the above methodology includes inter alia formal reviews of procedures and processes, analysis of complaints and incident reports and review of new products and services. The output is then used to update MCBCM’s risk maps, which address all major risks faced by the business and their pre-control ratings. These risks are eventually re-assessed taking into account existing controls and additional controls that are required to arrive at a post-control rating. Any residual post-control risks deemed material would lead to a re-design of the relevant controls until such risks are eliminated.