Financial Statements

Independent auditor’s report

To the Shareholders of MCB Group Limited

Report on the Audit of the Consolidated and Separate Financial Statements

Key Audit Matters

Impairment of loans and advances and debt instruments carried at fair value through other comprehensive income - application of IFRS 9 and estimates used in the calculation

As from 01 July 2018, the Group has applied IFRS 9 ‘Financial Instruments’ which requires the recognition of Expected Credit Losses (‘ECL’) rather than incurred credit losses.

The determination of ECL requires a fundamentally new and highly judgemental approach and relies on complex modelling and the use of a number of data points to determine the ECL on its stage 1 and stage 2 financial assets. The data has been sourced from a number of systems that have not been used previously for the preparation of accounting records. This increases the risk around completeness and accuracy of certain data used to create assumptions and operate the models.

Management is required to determine the ECL that may occur over either a 12-month period or the remaining life of a financial asset, depending on the categorisation of the individual asset.

Given the complexity of the PD, EAD and LGD models used for the ECL calculation, our actuarial expert team assisted us in performing certain procedures. With the assistance of our actuarial expert team, we assessed the input assumptions applied within those models by agreeing the key inputs used therein to the supporting documentation and independent extraction made from the system. The reasonableness of the forward looking information were independently verified, on a sample basis, to external sources.

Further, our procedures included assessing the appropriateness of stage 1 and stage 2 of the ECL model through independent re-performance and validation procedures. In addition, we tested the integrity of critical data used at year end to calculate ECL by verifying these to the relevant systems. We performed risk based substantive testing of the models, including independently rebuilding certain assumptions.

In connection with the separate financial statements, we have determined that there are no key audit matters to communicate in our report.

Report on Other Legal and Regulatory Requirements

Mauritian Companies Act 2001

The Mauritian Companies Act 2001 requires that in carrying out our audit we consider and report to you on the following matters. We confirm that:

- we have no relationship with or interests in the Company or any of its subsidiaries other than in our capacity as auditor of the Company and some of its subsidiaries, tax and business advisors of one of its subsidiaries and dealings in the ordinary course of business with some of its subsidiaries;

- we have obtained all the information and explanations we have required; and

- in our opinion, proper accounting records have been kept by the Company as far as appears from our examination of those records.

Other Matter

This report, including the opinion, has been prepared for and only for the Company’s shareholders, as a body, in accordance with Section 205 of the Mauritian Companies Act 2001 and for no other purpose. We do not, in giving this opinion, accept or assume responsibility for any other purpose or to any other person to whom this report is shown or into whose hands it may come save where expressly agreed by our prior consent in writing.

Statement of Accounts

-

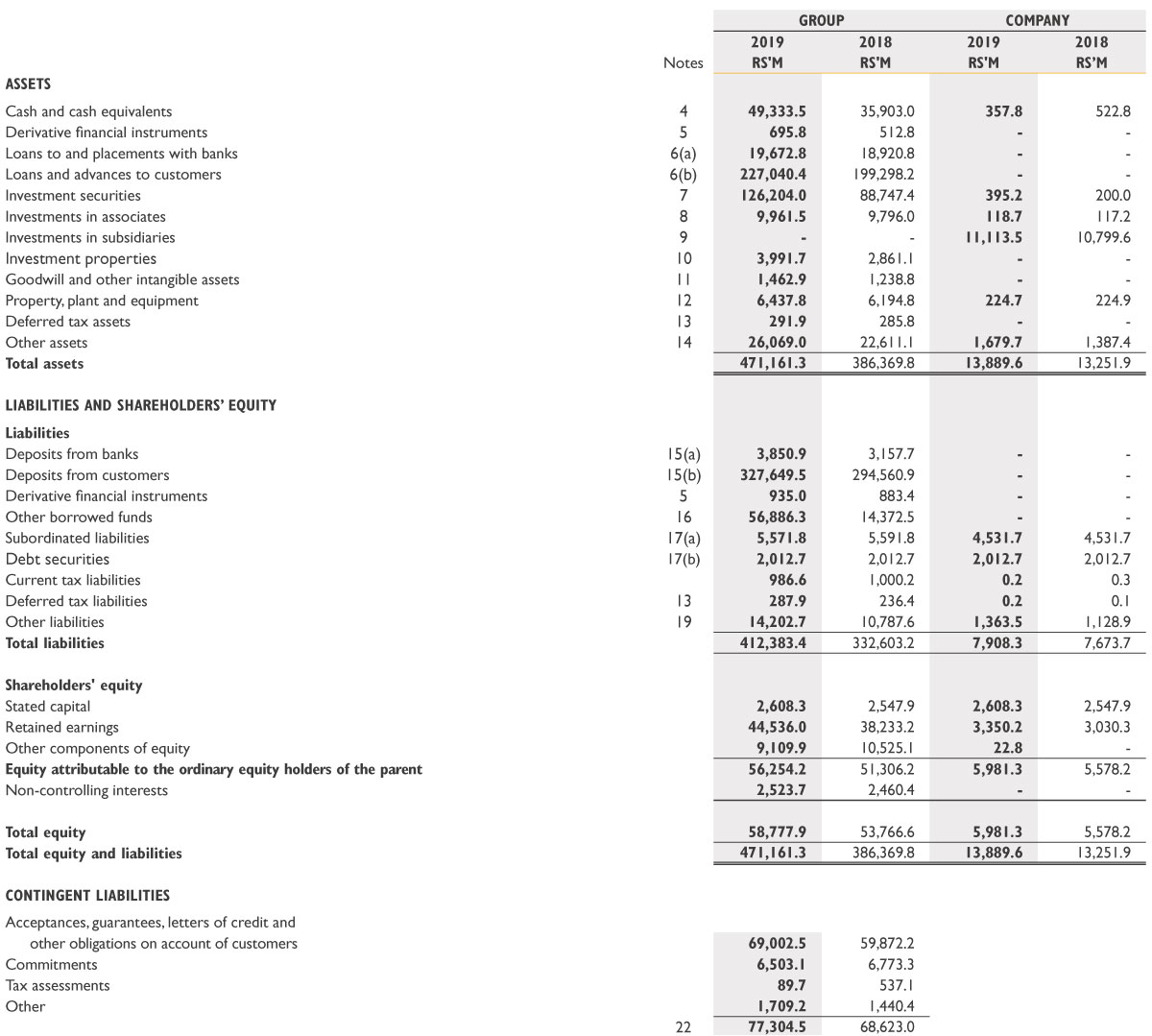

Financial Position

-

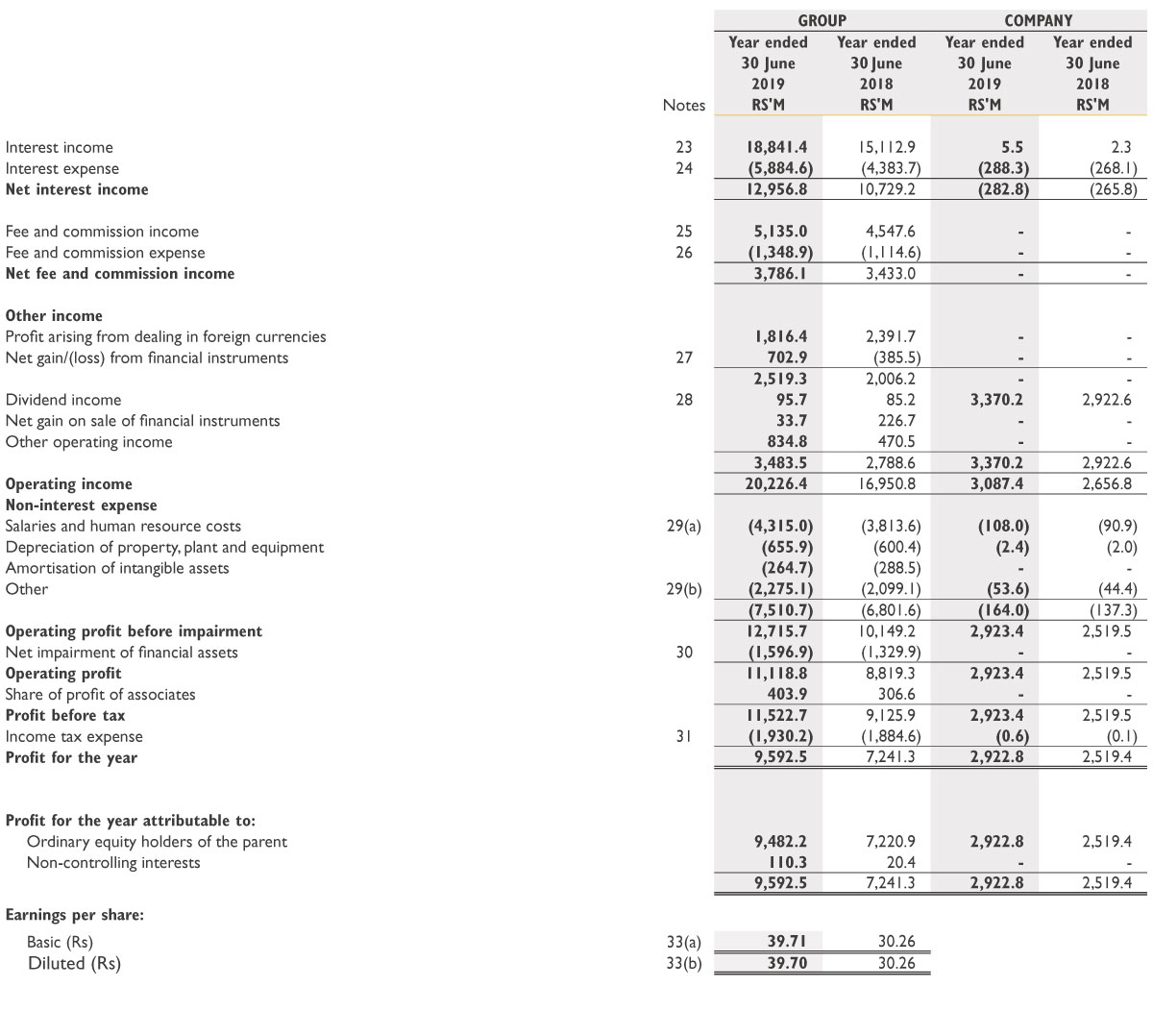

Profit and Loss

-

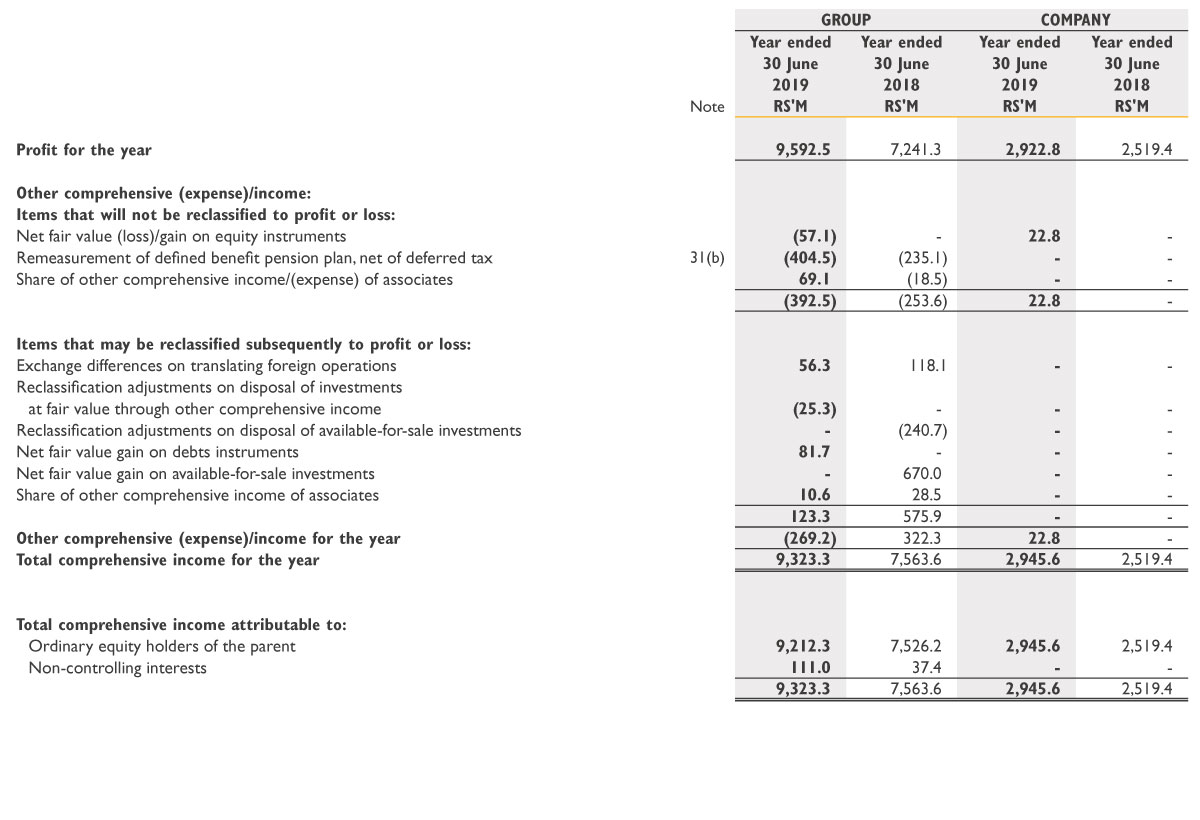

Comprehensive Income

-

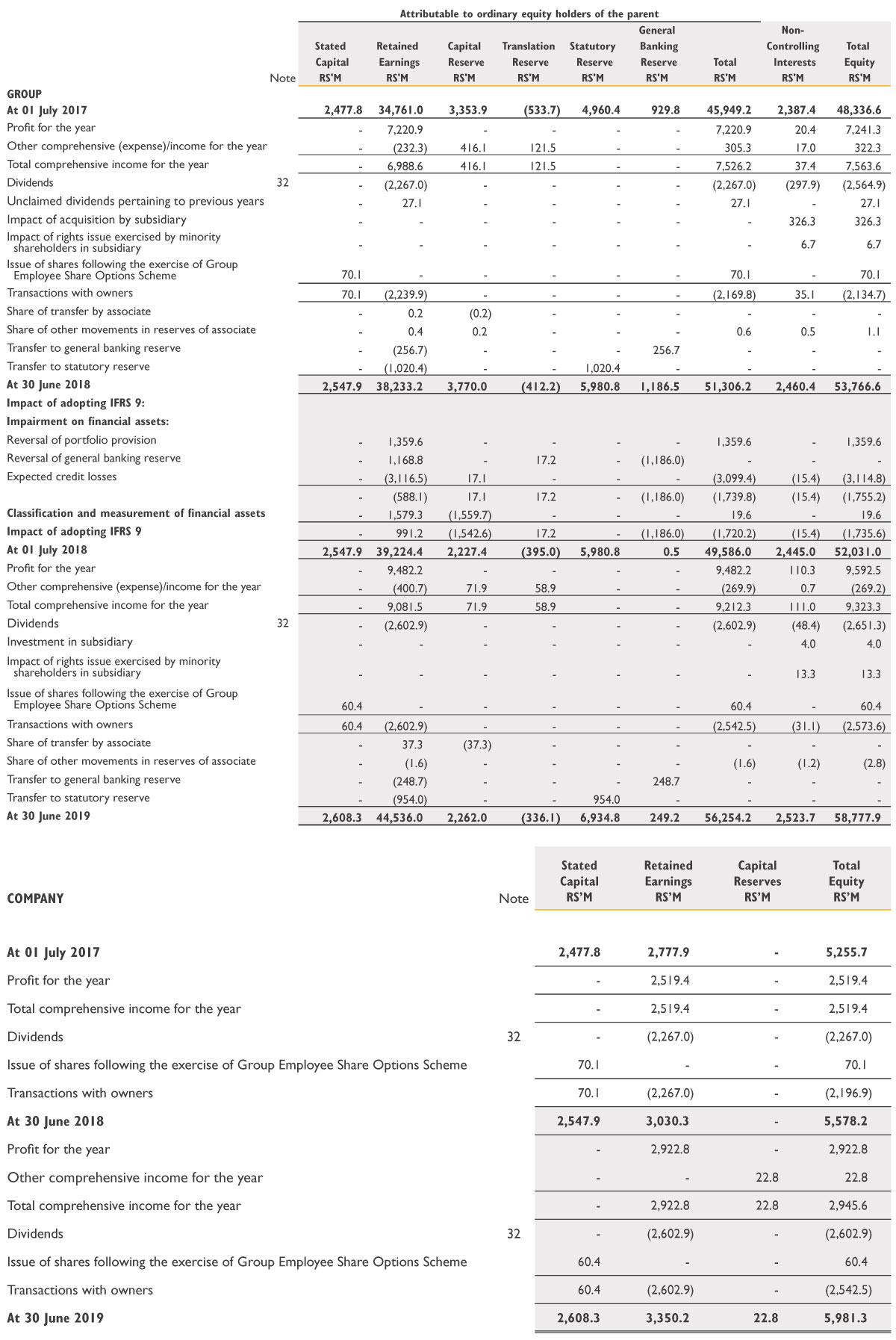

Changes in Equity

-

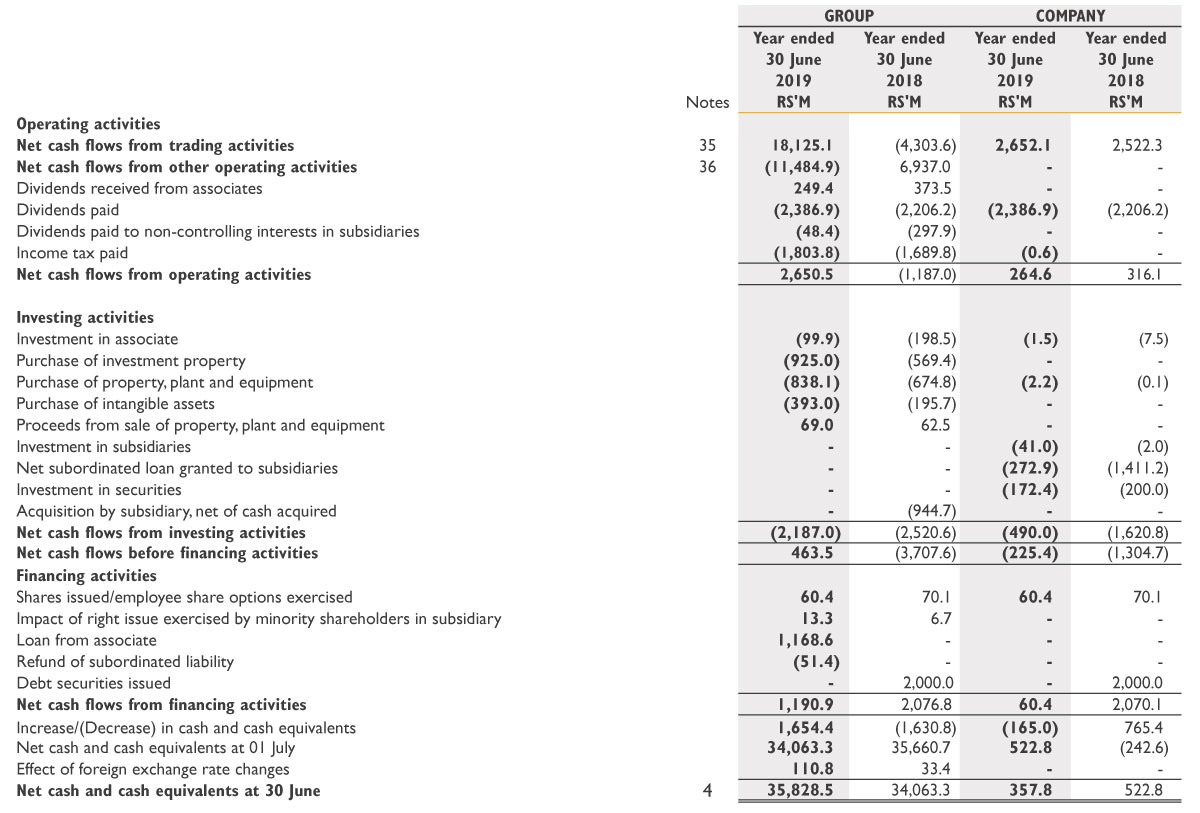

Cash Flow

These financial statements were approved for issue by the Board of Directors on the 27 September 2019.

The notes on pages 208 to 299 form part of these financial statements. Auditor’s report on pages 188 to 194.

General Information

The MCB Group Limited (“the Company”) was incorporated as a public company limited by shares on 05 August 2013. Its registered office is situated at 9-15, Sir William Newton Street, Port-Louis, Mauritius.

The Company is listed on The Stock Exchange of Mauritius Ltd.

The main activities of the Company and those of its subsidiaries (“the Group”) consist in providing a whole range of banking and financial services in the Indian Ocean region and beyond.

Index to notes to the financial statements

2019 in Retrospect